deutsche Fassung

Version en español

Русская версия

Version française

2.6. Cash Flows

The depiction of monetary flows was not given any special significance in the 1494 system. A presentation of cash flows was therefore not planned. In Anglo-Saxon countries this value was

emphasized. In addition to wealth, capital and success, the payments that are roughly allocated to operating, investing and financing activities should also be presented. Subdivisions are

useful.

If you want to observe the cash flows, the cash balances can be recorded in sub-accounts in order to record a (original) cash flow measured directly on the payments made according to the direct

method (corresponding to real life reality). IAS 7.19 recommends the direct method of receiving payments for the sale of goods and the provision of services, incoming payments from user fees,

royalties, commissions and other income, payments to suppliers for goods and services, payments to and for employees, payments and reimbursements income taxes and others in operating cash flow.

You can create subaccounts for the opening balances and these cash flows, which can be transferred to an account for the final inventory at the end of the year. However, the daily work would be

made more difficult because a comparison between the stocks according to bookkeeping and the actual cash holdings is very extensive. But with computer support this could be organized.

2.7. Cost Accounting

Although a cost accounting was already carried out by the trading house Fugger in the 16th century, the techniques were developed only after industrialization. The problem of Accounting 1.0 is

its one-dimensional representation. When posting to accounts, you have to decide on an outline criterion. However, cost accounting is about the entire value creation process, which spans from

input via production to output and thus has to represent these three dimensions.

An operating settlement sheet realizes two dimensions by assigning the cost elements (input) in a table to cost centres (places of value added = production) at the same time. The third dimension

can be created with a BAB II and an allocation of cost centres to payers (output). In the case of this tabular solution, accounts were subsequently manually evaluated in Accounting 1.0 and the

second dimension (cost centre) was added.

On the other hand, cost accounting on special accounts should allow immediate entry of cost centres or payers and thus be more accurate. With the concept of cost accounting in accounts, direct

costs that could be directly attributed to the products were posted to cost object accounts and the overhead costs, which could only be assigned to departments, to cost centre accounts. Then, the

cost center accounts should be distributed via the cost object accounts and then completed via an operating result account.

This type of costing and the determination of the results per cost unit involved disproportionately high expenses. The advantage that an immediate booking of the cost centres was made, however,

was low. It is understandable why this technology was not practiced by the companies at all, or for a very long time. Nevertheless, some terms of this technique (e.g., operating income account)

are still found in the textbooks, although their authors may not even know the old method.

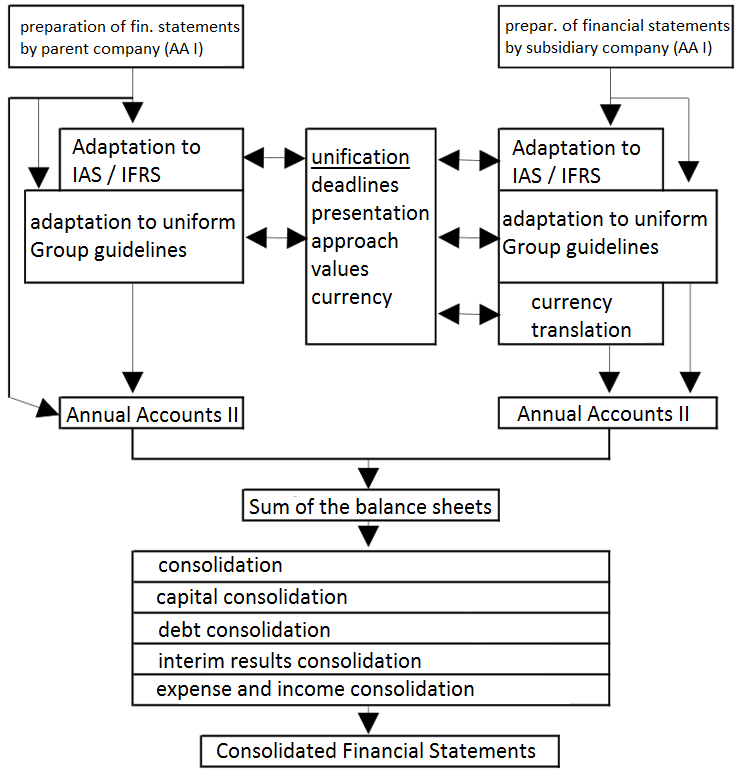

2.8. Consolidated Financial Statements

The distinction between legal and economic unity was of no importance at the time of Paccioli. Only with the industrialization and the emergence of the joint-stock companies also economically

dependent enterprises developed, whose stock majorities were held by other enterprises. First economic empires emerged.

A group is a group of legally independent companies that are under the joint management of a parent company. The bookkeeping is organized by the individual companies. However, the management of

the group and also the public have an interest in controlling the corporate group as an economic unit. For this purpose, in addition to the separate financial statements of the legally

independent companies, consolidated financial statements have been developed for the corporate groups. In them, the group is presented as if it were a legally unified company.

Fig. 7: Group consolidation

Source: D. Baukmann / U. Mandeler, International Accounting Standards:

IAS und HGB im Konzernabschluß, 2nd ed., Munich / Vienna 1998, p. 18

Especially with international corporations there can be different problems. Amounts in other currencies have to be converted and the accounting of the different countries can be organized

differently with different legal bases. Then, each group company must first prepare a financial statement based on the parent company's rules. This is not very easy if the bookkeeping continues

to build on its own rules. The uniform financial statements according to the rules of the parent company are referred to as Trade Balance II.

Thereafter, the trade balances II of the entire group of companies are added up to the aggregate balance. However, this also includes transactions that took place between the Group companies and

that would not have existed in a single company. The parent company also accounts for the interests in the group companies that would not exist in a single company. The equity of the Group

companies is also included in the aggregate balance sheet; but in a single enterprise this would not happen. This separation of internal processes from the figures of the group of companies is

called group consolidation.

Group consolidation is to be tabulated in Accounting 1.0. A group accounting is not planned.