deutsche Fassung

Version en español

Русская версия

Version française

6.1. concept

Who cannot see well should not drive a car! Who has no accounting should not lead a company! Both would drive the cart to the wall!

But in developing countries, the average microenterprises do not have accounting and they cannot be expected to be bureaucracy. But well-functioning small businesses are an important factor in

the emergence of small and medium-sized businesses. However, a broader middle class is an important factor in the development of a local economy that could make these countries more independent

of world markets. A stable local economy is the most effective way to fight the causes of flight.

The necessary information for good corporate governance is the monthly data of a balance sheet, income statement and cash flow statement, as well as a simple cost and activity accounting with

cost element accounting (especially with the calculation of imputed costs), cost center accounting (for cost control) and cost unit accounting (for the price policy and product policy). From this

it should be possible to develop a plan for the future.

It is estimated that small businesses need business support. A local or regional cooperative could use multitenant ERP software that reads simple data entry from members into a spreadsheet,

processes it automatically, and provides professional analysis to its members. An economically trained employee of the cooperative would have to look at the evaluations and draw the members'

attention to opportunities and risks.

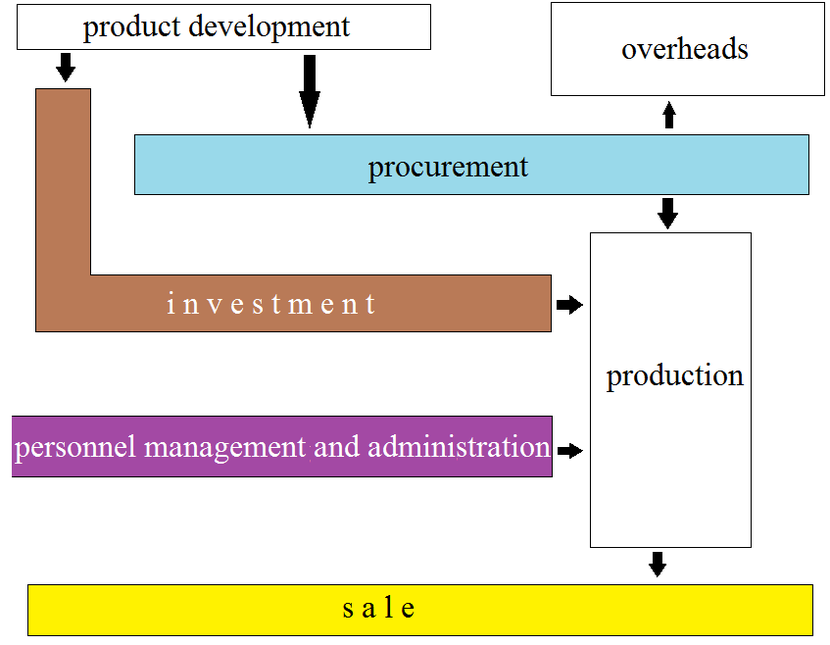

Fig. 52: Value added and ERP (core area)

(Source: own illustration)

The target group is very strongly oriented to the cash flows. A book keeping in German tradition, which creates a balance sheet and P & L account from a complex bookkeeping and derivatively

determines the cash flow, comes from acceptance problems. The reverse method is to be used to derive a profit and loss statement from cash flows in connection with a balance sheet. However, the

inventory of fixed assets, inventories, receivables and cash and cash equivalents as well as liabilities from operating activities and financing must always be legible. It would be very close to

simple accounting. Nevertheless, a simple cost calculation should be possible.

The analysis of the value added processes from Fig. 22 on page 95 and their refinement in Fig. 23 on page 96 must first be reduced to the core area, for which work aids with spreadsheets should

then be offered.

This should produce the necessary data overall.