deutsche Fassung

Version en español

Русская версия

Version française

4.1. System

The term "accounting 3.0" is in contrast to the two chapters previously somewhat problematic, because the approach is greatly expanded, was beyond an accounting in the strict sense. Much of the

accounting 2.0 is also simply transferred and integrated into a larger context. In these parts the renewal does not go very far.

However, the name can be justified with the function of accounting as a navigation system of the company management. Just because the other elements are included in this navigation system is a

new quality. At the name as accounting you should not bother then.

4.1.1. philosophy

Accounting is a model of the company. The model concept can be distinguished several times. Thus, e.g. Oldtimer miniatures, three-dimensional representations of a new construction project or also

simulations of climate researchers as models called. These can still be distinguished in explanatory models and decision models, which the o.g. Examples can clarify. The classic car miniature is

an explanatory model because it illustrates the appearance of a car of the past. By contrast, the presentation of a new building project serves as a decision model for the presentation of the

future. Several variants of the future can be compared with it to decide for the best. Models do not have to be real, but like the climate model, they can also be virtual. Virtual models, as

combined models of explanation and decision making, can explain the causes of observations of the past and, on this basis, simulate future developments (for example by reducing CO2 emissions).

Thus, these models serve to select the decisions that promise the most favorable development in the future.

There is a tendency to constantly refine the models. This also applies to the model representation of the company, which was previously a virtual number model of financially relevant sizes. Even

at the time of Paccioli, however, it was possible to distinguish between the working level and the evaluation level in accounting. The preparation of evaluations was tedious and so dominated the

provision of data for daily business. At the working level, the data was generated that was used at the evaluation level. With the use of EDP many evaluations were constantly available. The

evaluations could be carried out at ever shorter intervals. At the same time, the working level was more efficient.

Against this background, all operational processes are to be recorded today. The accounting is to be expanded to the memory of the company. As in human memory, a distinction must be made here

between important and unimportant. Therefore, the operational processes must first be known. This then recognizes the information that fits into these processes as important.

With the extension to the whole company, goals are also controlled with the procedure from Fig. 12 on page 70, which do not have to pursue any economic goals. This allows the company to set

environmental goals and set up a reporting system to control the achievement of this plan.

The graphic on the front page for this chapter says that many of the organizational and technical tools that do the hands-on work flow into the ERP. The graphic names the task areas:

Business Intelligence Production Supplies

Logistics Purchasing

Sales

Personnel / HR Construction

Planning

Investment and Finance Controlling Accounting

There are own software solutions here. They are coordinated in an ERP system so that data can be transferred to other applications and all information from all applications can be viewed

everywhere. Of course, with authorization codes, access can also be restricted for security reasons.

4.1.2. volumes and amounts

A major change compared to the accounting 1.0 and 2.0 is the consistent combination of volume and monetary units, as long as it cannot be in terms of financial assets, as in the case of claims,

liabilities and means of payment. But even here, inflation could be eliminated by using units of measure.

In the operative business, only the quantity unit is usually important. Procurement is about units of measurement of a variety of input factors that need to be in the right place at the right

time. In production, the planned quantity is to be produced in the planned time, for which delivery dates may have already been agreed with the customers. Also in sales it is in the sales

targets, so again by units of measure. If they are not reached, the whole operation suffers from underutilization.

Accounting 3.0, which intends to integrate all operational functions in ERP, must meet these requirements. At the same time, however, it can also automatically evaluate the quantities (quantity ×

value = amount) and increase the awareness of the persons involved in the economical use of resources.

4.1.3. past and future

The companies are not led in the past, but in the present with a focus on the future. The data on which the company management can rely, however, comes from the past. It is therefore the concern

of Accounting 3.0, to generate data for the future.

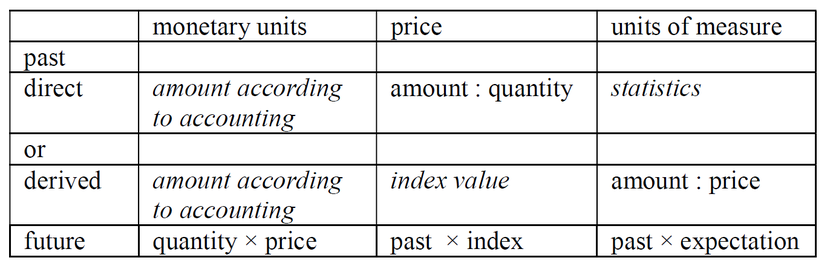

The available data is initially recorded in quantity and monetary units for past and future. The units of measure can be entered directly or derived from the amounts. Both methods can be combined

depending on the nature of the processes. The future is derived from the past. The procedure can be represented as follows, where the italicized words are for entering data:

Fig. 21: Past and future

(Source: own illustration)

For the past, statistics on consumption, production and sales volumes are needed in addition to the amounts from accounting. If it does not make sense to carry differentiated statistics for individual consumption quantities, the level of purchase prices can be observed and the price development can be expressed in a price index. The derived artificial consumption quantities are then the consumptions based on the prices of the year in which the system was introduced. The values of the future are then an extension of the past. For the units of measure, an expectation must be formed, e.g. because a planned increase in the sales pays also mean higher production and then higher consumption.

4.1.4. Enterprise Ressource Planning (ERP)

The implementation of accounting 3.0 in companies is often a job creation program for management consultants. Software vendors only sell their programs and companies are overwhelmed with their

setup. The consultants, however, know the possibilities of the software, but not the processes in the companies. In the end, the introduction of ERP systems causes high costs and does not bring

the desired results.

An alternative possibility would be to set up an ERP system for a fictitious sample company. Companies could then copy this proposal and adapt it to their needs. In many cases, texts would have

to be changed. Rarely, completely new processes would have to be set up, which would not have been provided by the model organization. If there were many different sample organizations for

different industries, company sizes and legal forms, the fit would be comparable to ready-to-wear clothing, which will easily be worn by the masses of the population. This idea is to be deepened

in this chapter. The following figure refines the rough representation and prepares it for the ERP concept:

Fig. 22: Value added and ERP

(Source: own illustration)

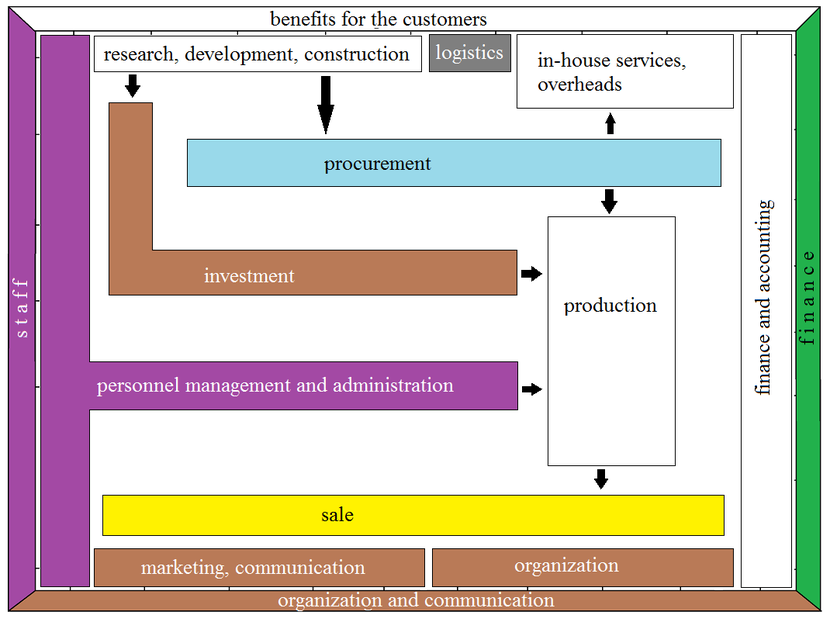

In Fig. 1 on page 9, the value creation process was roughly presented. Potentials and repeating factors (= investments and current purchases) are recombined in the production of products and

sold, whereby the production factor of labor in this process is incorporated and the use of capital makes it possible.

The individual rectangles are divided into different tasks. They are more or less networked with other tasks. This breakdown and networking is the subject of the remaining description of this

chapter. It can be understood as a catalog of requirements, which should be considered when programming. The processes in industrial companies form the mental background. But they are also

transferable to other industries.

4.1.5. Technique of description

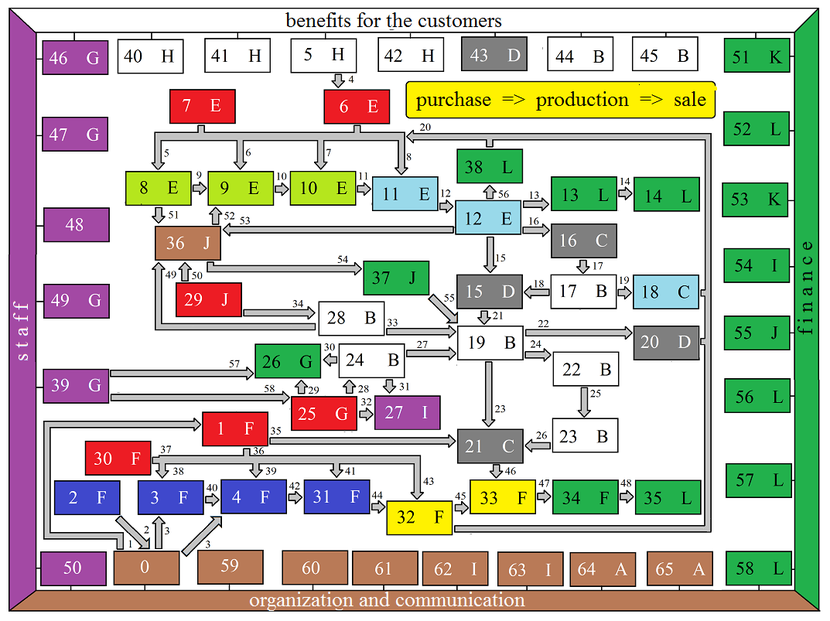

The breakdown of Fig. 22 on page 94 can be done as follows, which requires explanation.

Fig. 23: Networking of tasks and functions

(Source: own illustration)

This graphic and the following explanations describe the division of labor and information flow in a company that is similar regardless of the specific products and the industries.

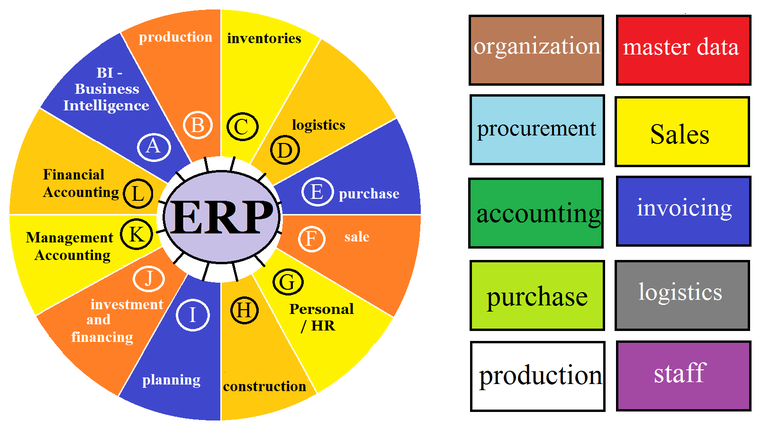

The letters in the rectangles of Fig. 23 on page 96 result in an assignment to the various functions of an ERP system according to the circle shown on the left; The colors used for the rectangles

have the meaning given in the rectangles on the right of Fig. 24.

Fig. 24: Explanation of Fig. 23

(Source: own illustration)

The numbers of the rectangles in Fig. 23 on page 96 refer to the sections of the following sections. The number is shown in brackets at the end of the title. These sections also explain the

arrows, which are also numbered.