deutsche Fassung

Version en español

Русская версия

Version française

3.6. cash flows

The desire to present the cash flows and their presentation or assignment to operating, investment and financing activities raises the question of how the data can be determined and how a

breakdown of the three cash flows can be made. Both are due, because a breakdown according to a certain criterion is only possible if the procedure provides the necessary data for it. It is

possible to differentiate between a primary and derivative approach as well as between the direct and the indirect method. The relationships to each other can be represented as follows:

Fig. 9: Cash flow procedures and methods

(Source: W. Müller, Investment Accounting, Financial Planning,

Financial Instruments, Norderstedt 2011, p. 92)

In the original procedure, the payment data is collected independently. This can e.g. This is done when booking any payment on sub-accounts. Another possibility would be to perform a database

export of all postings to the cash accounts, and to sort these completely exported posting records for different characteristics. For example, It can be determined from the counter accounts that

payments via customer accounts must concern the customer payments and those via vendor accounts the supplier payments. Other characteristics such as the document numbers or possibly also the

posting texts - if this was previously organized - can allow a classification. With a structured sequence of sorting processes more and more processes can be assigned.

Only a small remaining remainder would have to be assigned individually. The disadvantage of this approach is that the data is not available as an automatic expression from the financial

accounting software. If e.g. Subsequent corrections made, it would always be necessary to check individually whether this would also affect the presentation of the cash flow. This must be taken

into account in the process organization. The original approach would be an isolated solution in this form.

For these reasons, most companies prefer the derivative approach of deriving the cash flows from the accounting data. Thus, while the original approach is based on the entries in the cash

accounts, the derivative approach examines all other accounts, that is the sum of all offsetting entries. This is based on the knowledge that all postings follow the following triangular

logic:

Fig. 10: Triangle logic of posting records

(Source: W. Müller, Investment Accounting, Financial Planning,

Financial instruments, Norderstedt 2011, p. 93)

All transactions for normal business transactions take place either between the profit and loss statement and the cash flow, the balance sheet and the cash flow or the income statement and the

balance sheet. If two of these quantities are known, the third can be calculated because the sum of debit and credit entries must be the same. This logic can be limited to the three activities

(operational, investment, financing). Instead of assets and liabilities, the balance sheet is broken down into working capital, other assets and other liabilities. Thus, the triangulation logic

can be concretized as follows:

Fig. 11: Triangle logic in detail

(Source: https://mueller-consulting.jimdo.com/finanzen/investition/,

Download file I + F-7c.pdf)

Working capital consists in particular of inventories, receivables and liabilities. In the operational area, the income statement forms the focus. Non-cash transactions take place in working

capital, which also includes non-cash payments. Investment activity focuses on fixed assets, ie other assets. Financing activities, on the other hand, are shown under other liabilities. Non-cash

transactions in the case of investment and financing are recognized in the income statement. The vast majority of operating income and expenses will also be cash-effective in the respective

accounting period. Income and expenses may not be cash-effective, e.g. Income from the reversal or expense from the formation of provisions. Insofar as operating income and expenses are not

immediately cash-effective, unpaid income and / or additional payments for prior-year expenses increase working capital. If receivables from the previous year are additionally paid in and / or

expenses are not yet paid, the working capital is reduced by the reverse order, which leads to an increase in cash flow from operating activities.

Cash-effective income also arises from the return on financial investments or from neutral assets or the sale of fixed assets. They are usually not part of the operational area. Depreciations and

write-downs on fixed assets and marketable securities are non-cash, but are required to calculate capital expenditures. The same applies with the opposite sign in the case of income from

attributions, e.g. for value reversals. Interest income and interest expenses are generally cash payments and can also be presented in cash flow from financing activities. Additions to fixed

assets and marketable securities are recognized in the income statement and relate to cash flow from investing activities.

Additions and disposals of equity and debt capital (with the exception of working capital) are financing activities. Non-cash expenses and income (with the exception of depreciation) relate, for

example, to the setting in or draw of provisions

Only the cash holdings are excluded from this classification. Because the derivative approach captures the cumulative offsetting entries for payments, cash is used only to verify that the cash

flows have been recognized correctly and fully.

In accordance with International Accounting Standard (IAS) 7, operating cash flow is presented using the direct or indirect method. Because the operating activity is mainly reflected in the

income statement, the indirect method uses this evaluation. It first corrects expenses and income that are not attributable to operating cash flow and then takes into account changes in working

capital. The indirect method can not be used in an original procedure, because there is no P & L available in an independent calculation of payment data that could be adjusted. The direct

method depicts the operational cash flows as they occur in reality. This can also be organized in a derivative approach. There are no differences in cash flows from investing and financing

activities. Because these are not linked to the income statement anyhow, a conversion from the profit and loss account is not feasible here. These quantities thus also follow when using the

indirect method of direct logic.

According to these findings, cash flow evaluations can be generated automatically using the indirect as well as the direct method with a list generator and retrieved at any time.

3.8. Group Accounting

Accounting 2.0 also creates more opportunities for groups of companies. The data from the accounts of the member companies can be transferred to an unofficial accounting database of the group,

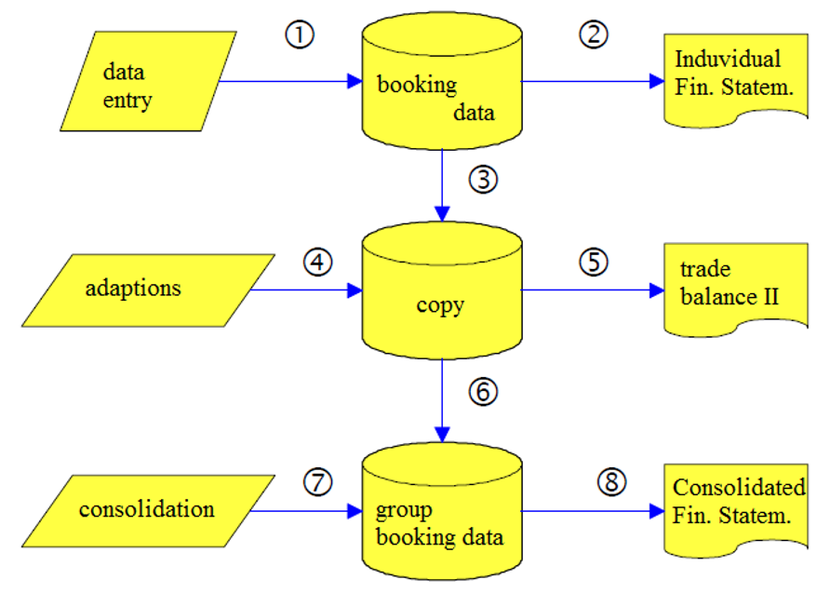

which can then produce its evaluations like those of a normal company. Based on the consolidation process (see Fig. 7 on page 30), this consolidated accounting is structured as follows:

Fig. 20: Group Accounting

Explanations:

(1) In the regular accounting all documents are recorded.

(2) The accounting data base forms the basis for the preparation of the individual financial statement.

(3) The bookings that have been recorded are reported i.d.R. Copied once a month to a second database. The data transmission can be done with the deposit of a second account no. respectively.

Thus, a group-wide chart of accounts for the consolidated financial statements can be used, whereby in the individual financial statements the group companies can continue to use their local

chart of accounts. This is particularly necessary in countries such as France, Belgium or Spain, which require their companies to have a mandatory chart of accounts.

(4) After each data transfer or at regular intervals, account maintenance must be carried out, which corrects postings that deviate from the standards of the consolidated financial statements or

from group-wide policies.

(5) This dataset forms the basis for the trade balance II. Like the separate financial statements, it is automatically generated from the accounts.

(6) At the closing dates (ie quarters), the updated data is transmitted to the head office. In most cases, this transfer is limited to totals and balances of the individual months according to

the group accounts. In the booking text, in the document no. or as a cost center, the transferring company is registered. All Group companies are then imported into a common database at the Group

headquarters. The cost center as identification of the group company then has the advantage that the group headquarters can reproduce the trade balances II of each group company via the cost

center module, which often spares queries to the group company.

(7) Consolidations in the narrower sense (see Chapters 4 + 5) are recorded at the Group head office as adjustment entries. The posting documents can also be created according to the logic of the

elimination method, in which each group company creates reports using the identification characteristic of intra-group transactions, which group-internal postings are contained in which accounts

of the trade balance sheet II.

(8) Consolidated accounting is the basis for the consolidated financial statements after the recognition of consolidation entries. It is automatically created from the accounts like the

individual financial statement.

(Source: W. Müller, the consolidated financial statements

according to IFRS, 2nd edition, Aachen 2005, p. 61 ff.)

If cost accounting is also to be consolidated by individual or all Group companies, the cost centre number in the booking file would not be available for the identification of Group companies. It

would have to be either in the group accounting a new field for a company no. be created, or the cost center no. would have to be provided in the group with additional posts. Then the cost centre

number in the group could be preceded by the company number.

A suggestion to solve the problem would be that the accounting programs in addition to account and cost centre (and possibly cost bearer) nor a project no. create as a free allocation field. It

could also be used during operation for spontaneous evaluations (projects) or e.g. in investment controlling for an inventory no. be used. That would be free in the group accounting in any case

and could for a company no. be used.

3.9. The bookkeeping of branches

The consolidation of accounting can also occur in the opposite direction. A company can have several businesses that all want to create and evaluate their own data. However, the bookkeeping

obligation exists for the company as a legal entity, ie for the sum of all enterprises. The company management also needs feedback at this level, even if the management of the individual

companies also needs feedback for their level. However, this need could also be covered by responsibility reporting in a central accounting department.

If a decentralized company also decides on a decentralized accounting system, where the decentralized services are also settled on a decentralized basis and the customers 'payments are made on

the bank accounts of the branches, who make their purchases on-site locally and pay their suppliers' invoices themselves, then a decentralized accounting would be consistent. Unlike corporations,

however, the transfer of individual records to a central accounting department would not only be an option but a legal obligation. The accounting obligation applies to the management. The store

would in their view be just a data collection unit and a repository for receipts. From the perspective of the branch managers, however, the bookkeeping should be as complete as possible, and

therefore also have a partial balance sheet and a partial profit and loss account available for each branch.

From a technical point of view, it would be no problem to export recorded bookings to a file that is read in by the head office via an interface. Organizationally, one would have to agree on

clear boundaries and deadlines in order to prevent coverage gaps and duplicate entries. To avoid such mistakes, it would also be necessary to create votes and controls.

A branch balance sheet would cover the local fixed assets, borrowed capital, own working capital and, in particular, cash holdings. For the initial preparation of such unofficial branch balance

sheet, the balance would be the pro rata equity of the branch. This would be continued with the pro rata profits from a branch profit and loss statement.

For transactions with headquarters or other branches, clearing accounts would have to be kept, e.g. if short-term liquidity assistance is to be repaid later. There are no expenses and revenues

between the companies. For this purpose, the highest special clearing accounts (for example, in equity) could be held, which cancel each other out. These clearing accounts should be closely

monitored.