deutsche Fassung

Version en español

Русская версия

Version française

3.5. Sub-ledgers

Digitization has had a particular impact on the Accounting 2.0. Because the coordination between sub-accounts and G / L accounts was now done automatically and a synchronization was guaranteed,

the possibilities widened. The usage was reduced to the question of whether the added benefit justified the additional costs.

3.5.1. Personal accounts and payments

The personal accounts were already provided in 1494 at Paccioli and are the oldest variant of sub-ledgers. In Bookkeeping 2.0, the application possibilities with the use of interfaces have

increased significantly. For example, orders are managed by customers in a merchandise management software and the invoices created for executed orders are first transferred to the accounting

department. The customer numbers must then match the customer accounts and the G / L accounts for sales and VAT must be stored in the ERP system. Otherwise, the merchandise management but more

concerned with the order processing of the offer on the order for delivery. That is why customer numbers are already being issued for potential customers who only asked for prices. From the

perspective of the seller, this is important information for the acquisition of new customers, from the point of view of accounting would be this garbage. For accounts receivable accounting, it

is still about the incoming payment control and possibly the reminder of overdue invoices and a response to the seller.

Comparable processes can also be provided by the merchandise management for the purchases. Because a preliminary run exists, from which the delivery date and the correctness of the delivery are

checked, a data transfer can take place here by interface, despite an incoming supplier invoice. This effectively transfers the data collection from accounting to purchasing, which then has to be

sensitized to the formal requirements. Here, too, there must be a synchronism of vendor and vendor numbers, and Accounts Payable Accounts may complete the data prior to the machine transfer on

the basis of the audited incoming invoice, and then organize payment by electronic banking.

These sub-books become independent. A transfer posting of the person accounts to G / L accounts could already be avoided in the accounting 1.0 with journal columns. Following the same logic, the

postings to personal accounts are simultaneously posted to accounts receivable and payable accounts, usually as a daily amount after the journal print. For this purpose, collective codes are

stored in the master data of the personal accounts, with which different collective accounts can also be accessed. These accounts must be locked for manual postings.

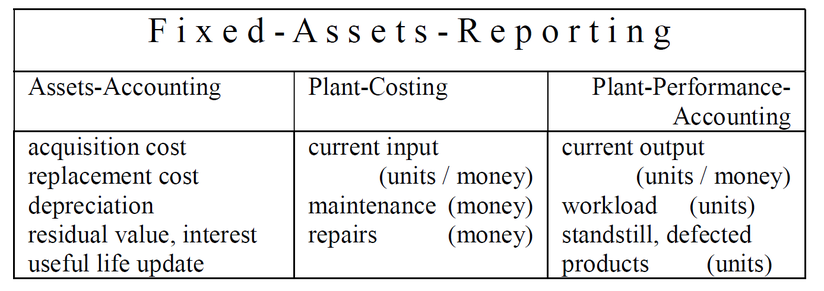

3.5.2. Fixed-Asset-Accounting

In section 2.5.4. was already mentioned Sect. 284 paragraph 3 HGB and the recording of the total acquisition and manufacturing costs, additions, disposals, transfers and write-ups of the

financial year and accumulated depreciation start and end of the fiscal year, the depreciation and amortization made in the fiscal year Depreciations in their total amount in connection with

additions and disposals as well as transfers during the financial year.

Fig. 8: Fixed-Assets-Reporting

(Source: own representation)

Because this is about managing investments, asset accounting is often expanded into asset reporting by adding investment asset-related costing in asset allocation and performance data in asset

performance accounting. All you need is a numbering system for the capital goods and a recording option in accounting and statistics. This will allow you to collect data for later replacement or

expansion investments and also to control your previous assumptions in order to learn for the future. At the same time, tendencies to calculate decisions are counteracted.

In Bookkeeping 2.0, asset accounting can be expanded into a complex investment controlling that would not be feasible with the 1494 technology.

3.5.3. Inventory Accounting

Inventory Accounting in Accounting 2.0 was able to recreate electronically the approach created in Accounting 1.0 with the quantities, price and amount. For purchases from purchases, the

quantities and amounts were available; the price (including pro rata ancillary costs) could be calculated. For disposals, quantity and price (as assumed value) were known; the amount for the

accounting was calculated. As with personal accounts, different goods can be assigned to a G / L account using collective codes. But there must be significantly more collection codes than with

receivables and liabilities.

Because the counter accounts (vendors in the case of purchases and material expenses in the case of sales or consumptions) are always the same, they can be stored in the warehouse accounting

software. Only cost centers and payers are different for the departures from the stocks. Purchases that are consumed immediately without intermediate storage can be booked as both an entry and a

simultaneous exit. The same applies to purchased services that are already physically non-storable. In this way, the inventory accounting can use the entire material expenditure (including

related goods and services) and the purchasing activity for this purpose.

As with manual stock accounting, the focus is on capturing purchased and used units of measure. However, the automatic processing of the data to the input of the operation allows the linkage with

output data on which the input quantities depend. Thus, input-output relations are determined, prognoses for the future and for simulations of different action alternatives are of central

importance. From this follows the desire to extend the "quantity-by-price logic" also to overhead costs, where the purchases are not recorded in the warehouse accounting.

3.5.4. foreign currencies

Foreign currencies in accounting 2.0 are an expression of globalization rather than the petty-bourgeoisie of the Middle Ages. With the introduction of the euro, the importance of foreign currency

accounting in Europe has shifted. For the countries of the euro area, the importance has declined sharply, while in other European countries (including non-EU members), the euro is accepted in

part (at least in border regions) as an unofficial secondary currency. Here, the processing of foreign currencies has become an important function of accounting. In addition to handling

international day-to-day transactions, a common currency is also important for reporting in international groups. In many high-inflation countries, value-stable currencies are often used for

reporting even without international integration. For the cash holdings, import and export transactions, the reference to the stock accounting has been preserved.

When reporting in foreign currency, all transactions from the national currency must be converted into the reporting currency. This raises the question of whether the conversion according to the

rates at the respective time of the transaction (time reference method) or whether the price on the reporting date (reference date method) should be used. This can have a significant impact on

the picture in the event of strong currency fluctuations (for example, the US $ as the reporting currency) or a strongly inflationary national currency. For example, In the case of the reporting

date method, an investment in local currency would be unrealistically low if the price of the reporting currency had risen sharply following the investment date. Both methods can be implemented

more technically, even if the time reference method is more complex. Here, the conversion rates must be updated daily or weekly. A second database must be maintained for the reporting

currency.

3.5.5. Payroll

The translation of payroll accounting into digital form is a simple task. You only need the individual records for the respective employees and periods. Now only the individual records are

printed as payroll; sorted by employees, they form the payroll accounts and sort the payroll journals by periods.

With machine processing, however, the database of the wage calculation can also be analysed. In production, it is registered which worker has been working on which product for how long. The

scarce resource work should be used effectively, and one work is ready, already waiting for the next task. This applies to all work, not just to the production of products for sale. It is now

also possible to determine which worker can perform the tasks faster and better. With this knowledge, everyone can be used primarily where it gives the best results.

In the pre-industrial era and the early industrial society, the production factor of labour was seen as a cost factor; Workers were easily interchangeable. In the late industrialized and

post-industrial times, staff are increasingly understood as a potential factor and thus as an investment. Simple work can increasingly be done by machines. Qualified workers must be trained and

trained. They are a prerequisite for the performance of companies. Payroll accounting should therefore develop in the direction of investment controlling.