deutsche Fassung

Version en español

Русская версия

Version française

6.5. cost accounting

6.5.1. cost units of craftsmen

The calculation of the orders is already provided in the order processing. In most cases, cost accounting is limited to capturing overheads for the entire operation and monitoring cost recovery

from labor and labor margins.

Something else can apply to builders who accept as well as minor repairs and complex construction sites as an order. For this, cheaper unit prices are offered in relation to the work done. In

return, the contractor has a basic load for a larger order, while small repairs also cause idle times. An ideal combination would be if large orders with generous deadlines represent the basic

load and then personnel can be deducted as needed for economically worthwhile minor repairs, so that there is no longer idle time. Because the large orders require price concessions, the

determination of long-term cost-covering prices and price lower limits is important. Would be offered because of a short-term underutilization very low prices, the normal price demands later

would have to be elaborately justified at a normal load.

The reference quantity for the overhead costs would be the working hours used. It would be recorded separately for small and large orders. Overheads that only apply to large or small orders would

be recorded in an appropriate cost center. For all other overheads, a general cost center is sufficient.

6.5.2. cost units of the taxis

The taxi drivers distinguish single trips in the city and overland trips. For single journeys in the city a higher price is demanded at night, which is based on a calculatory night supplement for

the own work force. Individual drivers also work day packages within the city. For tourists, it is usually cheaper to do single trips with different drivers. The drivers can only calculate the

variable costs for an average route and cover the fixed costs of the day with the remaining contribution margin. The profitability of the operation depends on the number of trips. With longer

waiting times is expected.

During a trip overland, the driver calculates the price from the variable costs for the route and the lost contribution margins of the day. The advantage is that it is safe to use, while during

daytime driving there is a risk of underutilization. On special days with a high passenger volume, the driver would rather not accept overland travel.

6.5.3. cost units in trade

In the trade a backward calculation according to the system of the division calculation is possible. With different cost centers, a multi-level division calculation can be organized. The

difference between buying and selling price can be determined easily. After deduction of the tax on services, which is calculated from the sales price, the margins of the various products result.

Retail selling prices in Cuba are subject to state price control. In other countries, a small retailer needs to be price driven.

The overhead of a month or year can be downscaled to a week or a single day. The margins of a week or a day must cover these overheads and additionally generate the profit. Because selling prices

can not be fixed arbitrarily, profitability must be improved through an increase in sales or with cost savings.

In retail, parts of the salesroom can be defined as cost centers. So should products with special requirements, e.g. Cooling equipment to cover these increased costs with additional margins.

Products with more space need to cover a greater part of the cost of the showroom because, alternatively, more products with a small footprint can be offered. Products that need to be picked up

by the supplier must generate the additional transportation costs that the supplier has already considered in his price when delivered to the retailer.

In wholesale, it is possible to differentiate between product groups or customer groups with different costs by means of a cost center number.

6.5.4. cost units in restaurants

A restaurant had the peculiarity that during the day the normal restaurant business was running, while in the evening music was played and only drinks were sold. The kitchen was closed. The load

was not very high during the day, while many visitors came in the evening. Here also less personnel was needed; On the other hand, the margins from the beverage sales were lower. The

profitability of the various activities can be observed with the cost accounting.

For drinks, the bar has to be based on the prices of other restaurants. A surcharge calculation can be carried out to determine cost-covering prices, whereby the required prices (= market prices)

should be higher. There would be two cost centers for the restaurant and the bar. The rooms would be assigned to an auxiliary cost center, the costs of which would be distributed to the two

activities according to a suitable key. The overhead costs of the bar would then have to be added to the purchase prices. These overheads and overheads would once again be topped up for general

overheads and another for the service tax.

In addition, a backward calculation according to the system of division calculation is possible. As in the trade, the difference between the purchase price and the selling price can be

determined. After deduction of the tax on services, which is calculated from the sales price, the margins of the various products result. The proportionate overheads one day could be divided by

the average margins. This would calculate from what sales volume the bar operation generates profits.

In the restaurant business, the purchase prices of food are low. The working hours for the different dishes can be different. However, because the cook processes several orders at the same time,

the working time for a single dish can not be determined reliably. But relations can be estimated between different products. Because of the low cost of food, purchase prices are not considered

as a suitable reference for the distribution of overheads.

It was therefore proposed to divide the restaurant operation in the cost centers kitchen and service. The overhead costs of the kitchen can be distributed according to the equivalence number

calculation. One product is estimated at 100% based on the estimated preparation time, and the remaining products are estimated with allowances and deductions for shorter or longer processing

times. For cost center operation cost rates per customer are determined on the basis of the monthly serviced customers after the division costing. The cost-covering prices of the individual

courts result first of all from the individual costs of the ingredients, the overhead costs of the kitchen, which are distributed according to equivalence numbers, and the operating flat rates

calculated with the division calculation. This subtotal is added to the general overheads as a percentage and then to the tax on services.

In another restaurant, there was a weak bar service next to the busy restaurant operation. Here the same procedure could be used. However, the bar was seen as a side activity, where customers can

possibly bridge waiting times until a table is free. The operator does not have his own profit expectation from this operating part, which is why he does not want to observe the economic

efficiency separately.

6.5.5. cost units for short-term rentals

For short-term rentals, different sized or elaborately furnished rooms can be defined as cost centers. The higher fixed costs from the larger area or more complex equipment must be generated with

higher prices. Auxiliary cost centers can be formed for cleaning and laundry. The landlords are interested in longer periods, because the rooms are not cleaned every day and laundry is not

changed every day. From this, there are scope for discounts or bonus benefits for longer periods.

A separate cost center is necessary if breakfast is also offered. The purchased food and the (imputed) costs for the preparation must be taken into account here. The same applies to additional

services provided for in the bill. Some landlords ask their guests e.g. a bike available. The amortization of the acquisition costs must be covered by the fee. If the bicycle is granted as a

bonus for longer stays, redistribution between the cost centers may take place.

6.5.6. imputed costs

The imputed costs also follow the basic pattern "Quantity × Price". For depreciation, the quantity factor is "1: useful life" and the price factor is the current replacement value of a new item.

For interest, the quantity factor is the tied capital and the price factor is the interest rate. In the entrepreneur's wage, the amount is the amount of work employed (100% or less) and the price

is the lost salary from an employee's job or the salary of the replaced employee, or a combination of both. For rent, the amount is the area used and the price factor is also the result of lost

revenues or costs saved. For imputed risks, the probability of damage is the amount and the average expected damage is the price.

Calculated depreciation and interest have already been taken into account in the inversión.ods file. Depreciation can be based on updated data, which means that current depreciation can finance

current replacement investments. There is thus a cross-financing of replacement purchases from the depreciation of items that need to be replaced later. With the formula

current value

--------------------

remaining life

this goal is achieved. However, it will probably come in the last third of the planned useful life to significant deviations from the original plan.

The cost of capital tied up may be taken into account by first calculating a weighted interest rate on the loan interest and expected return on equity. Because all assets are financed from a mix

of equity and debt, the residual value can be multiplied by that interest rate. The imputed residual value results from the factor

useful life – period of use + 1

------------------------------------------

useful life

multiplied by the current replacement value. This calculation path has the formulas of the file mapped.

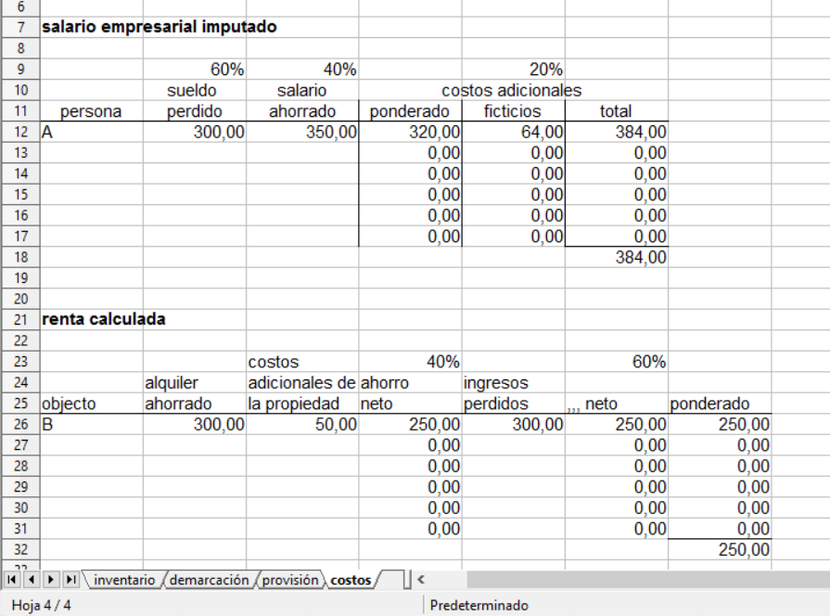

Fig. 98: Entrepreneur's pay and rent

(Source: download file - There is only a Spanish version.)

Calculated entrepreneurial wage, imputed rent and imputed risks are represented by the file valoración.ods. For the first two case groups, the imputed costs are calculated from lost revenues and

/ or costs saved with your own resource. The tables of the file have a weighting factor which can form a combined value from both calculation paths. The entrepreneur can also opt for either way

by weighting it at 100% and the other at 0%. The tables provide several lines for several co-entrepreneurs or several self-used objects. In the calculatory entrepreneur's salary the lost and the

saved salary is entered and weighted. This value is increased by the mark-up for staff costs, which would also be incurred for employees. At the calculative rent, the saved rent and the

additional room costs, which would not arise to a tenant, are registered. The difference is the net saving of the owner of the business premises. The second calculation method from the lost

rental income also deducts the additional costs and thus determines the lost net income from the non-letting. Both results are also weighted.

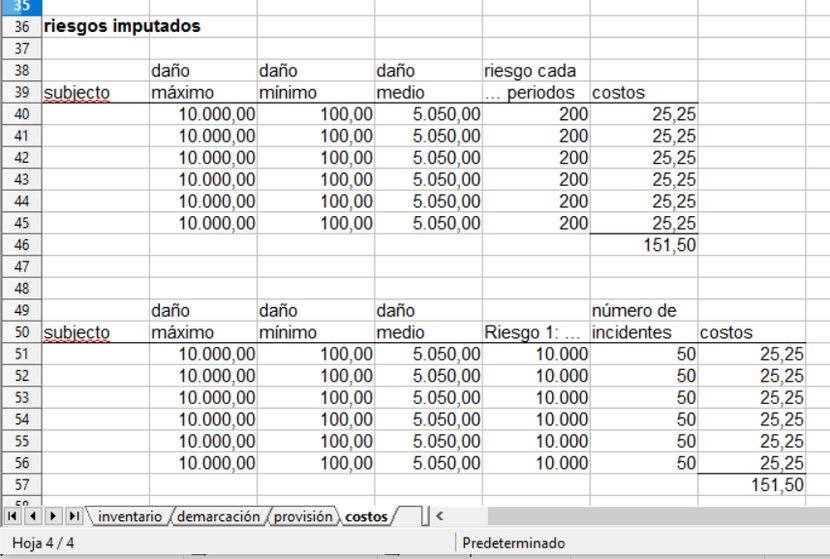

Fig. 99: Imputed risks

(Source: download file - There is only a Spanish version.)

For the imputed risks, a distinction must be made between volume and time-related risks. For periodic risks, the maximum and minimum losses are estimated in the event of risk occurrence, and then

average damage is determined as the price factor. The quantity factor is the number of periods in which the risk can be expected to occur. In case of probable damage in 10 years, the quantity

factor would be "1: 120". For quantity-related risks, the price factor is determined in the same way. The quantity factor results from the number of events that are to be expected to be damaged

multiplied by the number of transactions that are realized in the period.

If no damage occurs, the imputed costs are still recorded. If the risk occurs, the damage is treated as a neutral expense and not included in the cost accounting.

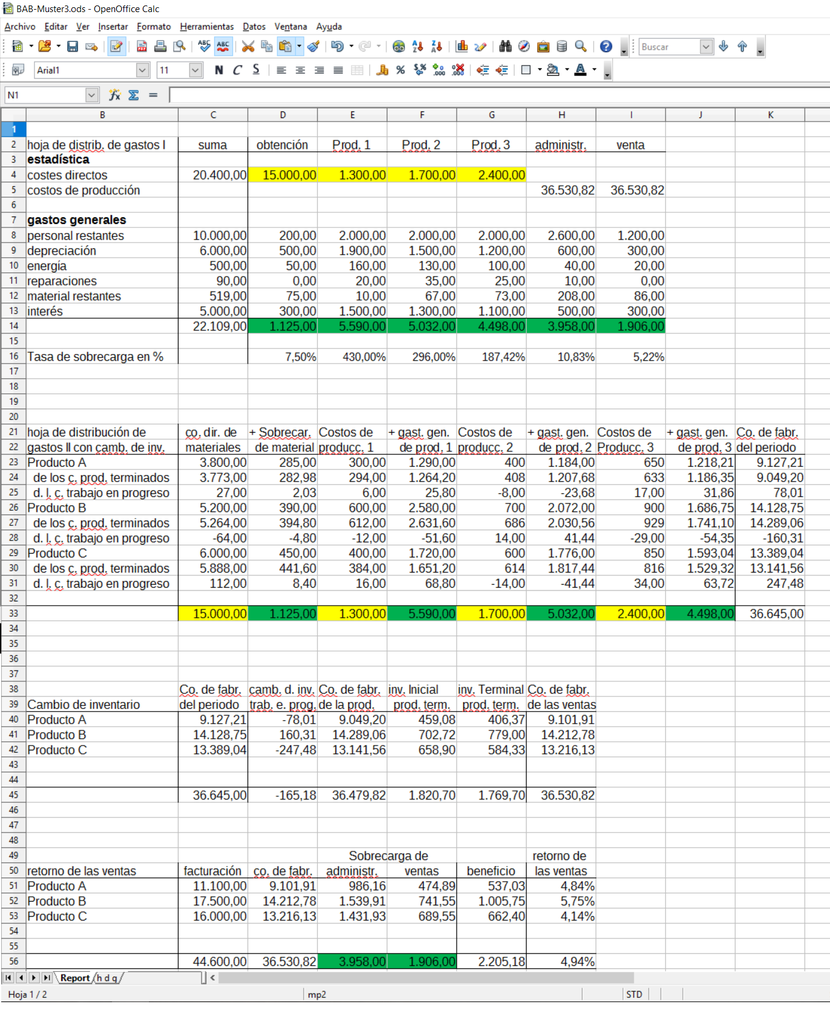

6.5.7. operating statement sheet

The operating statement sheet (BAB) is from the internal point of view a very important source of information for the company management. In BAB I, the distribution of cost elements is displayed

on cost centers (groups). This provides the basis for the distribution of cost centers to payers, the valuation of inventories of work in progress and finished goods and a product-related profit

and loss account. The database is a reporting system for the individual and overhead costs in the operational functions (= areas of responsibility => Responsibility Reporting) and one about

the sales and unit costs of the products or product groups (Activities => Activity Reporting).

Fig. 100: Responsibility and Activity Reporting

(Source: download file - There is only a Spanish version.)

Responsibility reporting covers all individual and overhead costs that are consumed in the respective area of responsibility. For corporate planning, the actual values will be extended into the

future. These data are mostly based on the evaluations of the annual financial statements. For the transition to the BAB I then neutral expenses should be kept as separate lines, which are then

not taken over in the BAB. Calculated costs can be included directly in the BAB I outside the Responsitility Reporting. In order to avoid manual data entry, this can also be done with a separate

table in the report worksheet.

Activity reporting not only reports on monetary units, but also on quantities produced and sold that are important parameters for day-to-day business. They relate only to finished products. In

the individual costs the costs of the period are reported and the line "of which finished products" (de los cuales productos terminados) is added.

The tables of the BAB I + II in the "hdg" worksheet contain only formulas that access the "Report" worksheet. The BAB I is based on the Responsibility Reporting and the BAB II with the

calculation of the inventory changes and the product profit and loss on the Activity Reporting.

In BAB I, the unit costs are managed as statistical variables that are used to determine overhead rates (in% of unit costs - last row). In the example of an extended BAB, production was

differentiated in three stages. In addition, the traditional functional areas of procurement, administration and sales were planned. The reference quantities for the administrative and

distribution overhead rates are the production costs of the products sold, which, however, are only calculated according to the BAB II.

The BAB II is divided into three tables. The first table lists the products or product groups in the rows and divides them into finished and unfinished products. It is assumed that the individual

costs consumed in the period and not included in the finished products have to be included in the work in progress. The direct costs are added to the direct costs using the overhead rates

determined in BAB I. The inclusion of changes in work in progress in the second table is therefore only a reclassification. The stock changes of the finished products are calculated from the

quantity data of activity reporting. The calculated production costs of the products sold are included in the third table, in which a product-related profit and loss account is constructed. Here,

the determination of profits is carried out in the horizontal instead of in the vertical. The lines now list the different products.

Fig. 101: Operating statement sheet I + II

(Source: download file - There is only a Spanish version.)

The profit situation of the individual products is the central information for the enterprise management. The system of BAB I and II (with the two other independent tables) shows how this profit

of the individual products is calculated. The operational processes, which are often seen as a black box, are thus presented transparently, even if some things are generalized and simplified.

Especially the small business owners have with this file a tool with which they can better understand their operation.