II Encuentro Internacional de Experiencias Empresariales

y de Investigación en Ciencias Administrativas,

21 y 22 de mayo 2020 - Bogotá

deutsche Fassung

Version española

Русская версия

Version française

The Open ERP Concept for Small Business

Experience report from a research semester in Cuba

submitted for the

II-nd International Meeting of Business Experiences and

Research in Administrative Sciences, May 21 and 22, 2020 - Bogotá

- canceled because of Corona

Foreword

After the first publication in 1494, in which Luca Paccioli described double-entry bookkeeping, little has changed for approximately 490 years. Rapid development began with digitization. With

Enterprise Ressource Planning (ERP), large companies now have a much larger and deeper database across all parts of the business.

Small business owners cannot be afford to work or invest in high-performance ERP software. For the most part, they also lack experience. However, they can capture the relevant data with a

template in a spreadsheet, to export a text file that can be uploaded to the multi-client ERP software on the Internet. After that, automatically generated assessments could be automatically sent

via email.

In the summer of 2019, the author prepared these templates for self-employed persons in the Guantánamo province in Cuba and offered them for testing. This outlines a way to create open ERP

software to support small business owners. The results of this project will be reported. In addition to the small and large business division, there is still a division between industrialized and

developing countries. Small businesses here are much smaller and their technical possibilities are much more limited than in industrialized countries. However, they are a pillar of the local

economy. The author believes that his conclusions are transferable to most developing countries.

At the same time, the work of Luca Paccioli from 1494 can be repeated under current conditions. ERP systems are treated as trade secrets of software vendors and business consultants who want to

sell their services. However, this knowledge must be made accessible to the world.

more information under https://mueller-consulting.jimdofree.com/research/

about the author https://mueller-consulting.jimdofree.com/home/person/cv/

1. Issue

“Who can not see well should not drive a car! Who has no accounting should not lead a company! Both are driving the cart against the wall!”

Fig. 1: Navigation system

(Source: https://mueller-consulting.jimdofree.com/research/history/)

Accounting has the task of a navigation system for the company. This is where the important information for corporate management is evaluated. This applies to large and small companies.

Digitization has created new opportunities for this, which are mainly used in large companies. The question arises how this experience can also be used for small businesses.

This text is not based on a literature review, but from the reproduction of your own observations in connection with a research project in Cuba. Because some of the colleagues at the University

of Guantánamo have not followed the instructions given by the management and they have to fear problems, the description of the experiences in the documents of a public conference must be very

cautious.

2. Background

2.1. Development of accounting technology

The double-entry system is over 680 years old. Accounting data from 1340 have been preserved in archives from Genoa. In general, this method is dated to 1494, when Luca Pacioli described it in a

book on Arabic numbers as a Venetian bookkeeping as an application example. There have been various approaches to simplify this method, but also to extend it, e.g. due to the expansion to cost

accounting, which has proven to be too expensive in practice.

Fundamental changes have taken place with digitization in the past 50 years. At first, the double entry bookkeeping was only reproduced on the computer. Before hard discs were invented, the

bookings were really registered in accounts and stored one after the other on magnetic tapes. The advantage over the entry on index cards was only that the tapes could be searched by machine.

Since around the mid-1980s, all data records have been stored in a single file, and the account number is only a sorting criteria. In many software solutions, the account number can also be

exchanged in order to have an accounting organization in accordance with national law in international groups, but at the same time to apply the rules of the group and to be able to evaluate the

data thereafter. For cost accounting, the accounts are assigned to cost types before data transfer that may be completely independent. In this way, profit and loss accounts for the individual

products can then be created largely by machine. There are also reports for individual areas of responsibility and business activities. This diversity would only have been inconceivable with

double-entry accounts.

For a long time, data acquisition remained a bottleneck. Documents had to be passed on in paper form from one desk to the next were they subsequently checked and stamped to ensure that. After

entering the data, it was available everywhere, but it took a long time to enter, which affected the timeliness of the information available. More and more interfaces were slowly being developed,

with which data generated or recorded in the company automatically copied into the bookkeeping. Manual data entry in accounting became more and more an exception and the quality of the data and

its timeliness improved.

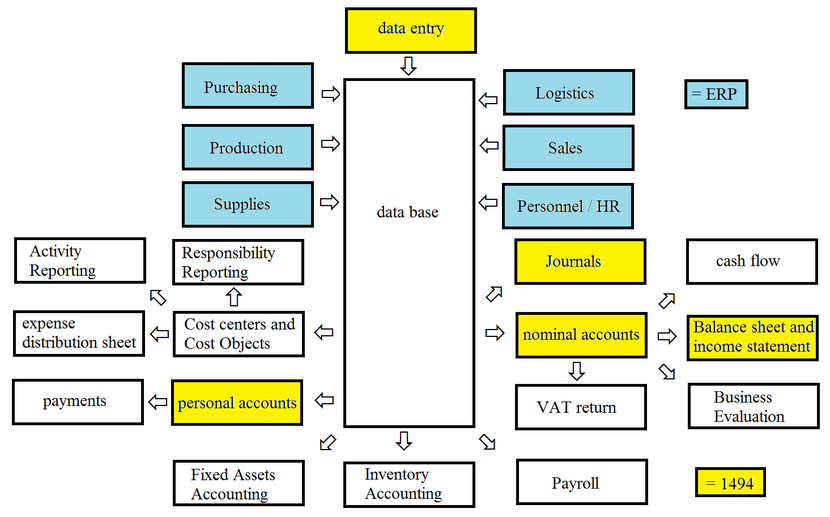

Fig.2: Accounting and ERP

(Source: https://mueller-consulting.jimdofree.com/research/accounting-3-0/)

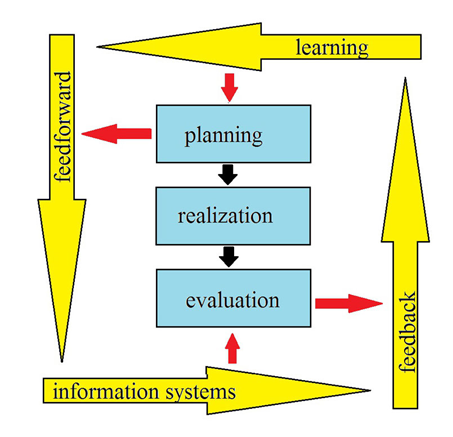

With the bulk of the data, the planning basis improved. With planning software and the definition of expected rates of change, different scenarios for future data can be simulated with reasonable

effort. Instead of being able to rely only on data from the past as before, companies with well-developed information systems have a comprehensive picture of the past, present and future. This

enables the company management to organize a continuous improvement process that combines a feed forward and a feedback with learning processes and information systems in a cycle.

Fig.3: Constant improvement process

(Source: https://mueller-consulting.jimdofree.com/research/idea/background/)

The complex information systems, which also include the outlook for the future, are known as ERP systems (Enterprise Resource Planning). They have prevailed in most large companies. However,

their introduction is often a job creation program for business consultants. Small businesses cannot afford this.

2.2. Small Business Solutions

Small businesses have also had computers since almost 30 years. Democratic business administration, which is geared to the interests of the masses and not a small minority, has to respond much

more to their needs than to those of large companies. 90% of companies in Germany have fewer than 10 employees. If the taxpayer finances science, it must give priority to 90% and not 0.3% of

large companies with more than 250 employees. Technical structures for small businesses that allow them to generate all the information necessary for good business management without expensive

specialists, can also be created.

At the same time, the industrialized countries should share their experiences with the rest of the world. Small and medium-sized businesses can create a middle class, which can also form the

basis for overcoming poverty in many countries in Africa, Asia and Latin America. Therefore, large and small companies worldwide should be provided with a good database for corporate

management.

2.3. Guantánamo

In summer 2018, the author was contacted via his website by a professor from the University of Guantánamo. In socialist Cuba there are strong income disparities that cannot be officially

explained. The country has an extremely large shadow economy, in which most small businesses also participate. However, the population believes that the main cause of inequality is corrupt

officials in the state sector, who in turn are good customers of the small business owners with their income. Since the beginning of 2018, there has been a campaign in the party newspaper that

criticized the quality of small business bookkeeping and accused them of tax evasion. In the tax law of November 21, 2012, Articles 58 and 59 provided for the application of the bookkeeping

obligation for small business owners, which was regulated in a very demanding manner by a regulation of the Ministry of Finance and Prices of December 30, 2010. However, the application was

suspended until early 2018.

The small business owners were neither technically nor from their knowledge able to guarantee complex double-entry bookkeeping. They had expected the deadline to be extended. The Cuban professor,

himself a member of the Communist Party, looked for alternative methods as a compromise to solve this conflict and came across a report from a research project that the author also had on his

website in English and Spanish translation. In a publication, the Cuban professor wanted to propose a simpler, computer-aided approach to accounting that could also be used to respond to the

party's criticism. The idea was developed for the author to organize a research project under his name and to report on it in Spanish on the Internet, which could then be cited in Cuba. Small

businesses were sought to test the data collection templates under his observation. A computer scientist at the university designed software structures with which the recorded data could be

transferred to a server via the Internet and processed there professionally and mechanically. With their spread, the shadow economy should slowly be pulled from the ground.

For the project, the author needed a certificate from the university with which he would have applied for a science visa. The Cuban professor found two young colleagues to visit the university

management during a preparatory visit with the author and to present the project. He wanted to keep himself in the background. The academic director of international relations saw the problem

that the small business owners are subordinate to the Ministry of Labor and that the university also has to apply for a permit there for the passive support of foreign research in this

field.

However, implementation could only begin after a change in the law in Cuba, which severely restricted the tax recognition of cash payments and made small businesses that had only been authorized

for a few years very unsettled. A discussion of this topic was no longer desired politically. The approval was not granted. The colleagues who supported the author towards the university

management were questioned by the State Security after his departure. Therefore the concept was changed.

Communication with two Cuban professors and some small business owners continued conspiratorially. From Germany, the author created templates for Open Office's spreadsheets, which small business

owners can use to collect their data and which would allow data to be transferred to professional software for further processing. During a later second visit with a tourist card, the author

inquired about the application experiences of the small business owners. The previously planned escort of the mission could not be carried out without the science visa. The small business owners

could only get technical help with the use of Open Office from university staff.

The concept for open ERP software, which was proposed by a university computer scientist, was no longer pursued by him due to the political pressure. At this point, the information should be

provided so that this concept can be accomplished by other computer scientists.

2.4. findings

The small business mindset is very cash flow oriented. The expenses and income of the income statement are too abstract for them. The investments made are concrete enough for them, but the other

balance sheet items are only perceived as future cash flow. This consideration should be noted and should not be criticized. Instead, the question must be asked how, with this cash flow-oriented

approach, the necessary data can be generated in order to make a navigation system available to small businesses too.

3. Open ERP concept

3.1. technical-organizational approach

The private sector, and in particular the small entrepreneurs described as workers on their own account, are of considerable importance for the Cuban economy. On December 16, 2018, the National

Director for Assistance and Control of Workers on Own Accouint of the Ministry of Labor and Social Security in Radio Rebelde stated that 589,116 people were self-employed at the end of November,

of which 171,126 were adolescents and 199,888 were women. (https://www.cubahora.cu/economia/trabajo-por-cuenta-propia-una-cronologia-de-preguntas-y-respuestas) This group is preceded by the

enforcement of the statutory accounting obligation, which was suspended until 2018 significant problems. With the approach now presented, these problems should be solved.

With the Open ERP concept, small business owners could record their data in a system that was adapted to them. From this, a file would have to be created, which you can up-load regularly to a

server via the Internet. There the evaluations would be generated, which would give them the necessary help for the company management. Shortening and simplification are also necessary, but

should not distort the essence of the statements.

Cuba is consistently expanding its Internet. Before taking office in 2018, Cuban President Miguel Díaz-Canel described the Internet as a "right for everyone" that had to be "made better and more

available". All Cuban provincial capitals now have LTE coverage. The new technology was built one year after the mobile Internet was put into operation with Chinese help and ensures significantly

better transmission rates than at the WiFi hotspot or at home. It is set to become the new standard in rural areas in the coming years, as the Cuban telephone company ETECSA announced. According

to the ranking of the company "Speedtest", which operates the app of the same name for measuring speed, Cuba has had the second fastest mobile internet in Latin America since October. The mobile

network is only faster in Uruguay. (https:// Amerika21.de/2019/12/235503/mobiles-netz-kuba-touristen; Dec. 17th, 2019)

However, because the prices are relatively high by European standards and especially against the background of Cuban incomes, online processing is out of the question. Log-ging into a website and

uploading a file would still be affordable.

A problem that should not be underestimated is the low level of trust that small business owners have in government institutions. According to the political definition, workers on their own

account are working class and organized in the trade union. Nevertheless, there is a natural conflict of interests between the profit-oriented small entrepreneurs and the state companies

fulfilling a supply contract. The union is therefore not really recognized as an advocacy group. In this situation, only a part of the transactions appear in the offi-cial accounts. This is why

small business owners fear that the data uploaded to a central computer will be checked by the authorities.

Even if the fight against the shadow economy is fundamentally a legitimate interest of the state, it would be counterproductive at this stage. The measures taken so far have ra-ther stimulated

the imagination of small entrepreneurs to hide the real scope of their business and damaged the honesty of entrepreneurs. To stop this dynamic, it would prob-ably make more sense if independent

business associations could also be formed as polit-ical interest groups, which would have to be given full control over the accounting soft-ware to be used.

Political advocacy should ensure that honest work is not made impossible by bureaucracy or excessive taxes. In return, an independent business association would build group pres-sure not to gain

an unfair competitive advantage through illegal practices. An automatic evaluation of the data and business advice under the full control of the association would, in a next step, point out to

the small business owners that the data would suggest that part of the business could not be recorded in the accounts and that effective advice would re-quire complete data.

Only then the state could gradually regain control of the private economy. After an intro-ductory phase with a voluntary participation in the system with simultaneous exemption from further

accounting obligations, compulsory membership could be introduced, while the politically independent self-administration should be retained. Only in a last step could electronic tax audits be

carried out by the tax authorities, as they are now common in Europe.

Politically independent business associations would then still be in the interest of the government. Their board members must have the trust of the members and they would also be committed to the

common good in the socialist economic system. They could then act as an intermediary, represent the interests of small businesses to the government and promote the economic goals of the state

among small businesses. Without this coop-eration, the enormous scope of the shadow economy would be preserved and with it the economy could develop legally.

3.2. regulation

The application of Articles 58 and 59 of the Taxes Act from 2018 has tightened the requirements particularly for small businesses. The regulations were already provided for in the law of November

21, 2012, but the application was suspended before 2018. Cuban small business owners are also subject to an accounting obligation. It is the basis for their tax returns and starts with an annual

income of CUP 100,000 = USD 4,000, even if the line is only exceeded in the current year. If the income falls below the line, an exemption from the obligation to keep accounts can be applied for.

In Germany, small business owners with sales of less than EUR 600,000 and a profit of less than EUR 60,000 are exempt from the accounting obligation. A simplified balance sheet applies to cafes,

restaurants, the trade in food and non-alcoholic beverages, and the manufacture and sale of shoes. The Ministry of Finance and Prices can, by ordinance, mandate accounting for individual

industries regardless of income.

In total, the self-employed persons referred to in Law No. 113 (Tax Act), for whom no simplified accounting applies, must keep 22 accounts, in addition to checking the income and expenses, the

financial statements, property, plant and equipment, material and personal accounts as well as a business accounting (Progreso Semanal, https:

//progresosemanal.us/20180227/activan-contabilidad-simplificada-actividades-privadas/, 16.05.2018) and payments must be made for the tax credit from a bank account. The annual accounts must be

prepared by January 15th, German companies have a deadline of June 30th.

Accounting is not specified in the tax law, but in Resolution 386 of the Ministry of Finance and Prices (MFP), which was published in the Official Journal on December 30, 2010. The resolution

sets out three Cuban accounting standards for the banking system, the national financial system and the self-employed in three documents. The basic objectives and criteria of the annual financial

statements as well as the compulsory chart of accounts for self-employment are presented in annexes. This scope can no longer be managed without professional support. According to both texts, the

accounting can be managed manually or via computer programs, whereby it is expressly stipulated that the self-employed must keep the information in one of the formats used for at least five years

in order to be checked at any time. The state-owned company CITMATEL offers the Administre su negocio and Cuadre applications, which are aimed at the self-employed and the non-governmental

sector, but which cannot be handled by small businesses because they are too complicate. One can assume that these programs were developed by computer scientists and that they did not ask the

workers on own account about their needs.

In fact, the 2013 tax law made only a few changes to previous resolutions by the Ministry of Finance and Prices that were not implemented. Articles 58 and 59 of the Taxes Act have remained

"frozen" since they entered into force in January 2013. Since then the government has been experimenting with accounting systems for private companies. When an improvement for self-employment in

Cuba was announced in mid-2017, the government linked this with the activation of Articles 58 and 59. Although there was actually enough time to adapt to the situation, this measure caught the

majority of small Cuban entrepreneurs unprepared.

Resolution 386 contains the "specific accounting standard for work on own account No. 1 - Presentation of the annual accounts" (NTCP 1), which sets out the minimum structure of the accounts in

Nos. 26 to 31. No. 26 regulates the balance sheet, which consists of three parts in tabular form. It must contain at least the following lines:

a) ASSETS

a. Current assets

i. Cash

ii. Bank balances

b. Net property, plant and equipment (property, plant and equipment less accumulated

depreciation)

i. Furniture and equipment

ii. Less accumulated depreciation

c. Total assets

b) LIABILITIES

a. Short-term liabilities

i. Fees, taxes and contributions payable

ii. Short-term bank commitments

b. Long-term liabilities

i. Long-term bank commitments

c. Total liabilities

c) Net equity

a. Balance of TCP equity at the beginning of the year

b. Increase in TCP contributions in the accounting year.

c. TCP expenditure in the accounting year.

d. Personal income tax payments.

e. Contribution to social security.

f. net profit

g. Total net capital

The balance sheet is therefore basically a combination of a balance sheet in accordance with IAS 1.54 with a statement of changes in equity in accordance with IAS 1.106, which in other countries

only publically listed companies present.

No. 28 regulates the minimum structure of the income statement, which follows the system of the nature of expense method in accordance with IAS 1.102; the function of expense method according to

IAS 1.103 is not permitted. It must contain at least the following lines:

sales

minus direct operating costs

Raw materials

fuel

electrical power

Remuneration for employed staff

Depreciation on property, plant and equipment

Other monetary and financial expenses

taxes and fees

Sales tax

Tax on public services

Tax on labor deployment

Other taxes and fees

Profit or loss in the company

A cash flow statement as in IAS 7 is not required in NTCP 1.

According to No. 29, an operating expense is recorded when there is an outflow of funds or the depreciation of property, plant and equipment is accumulated for the period. Lease payments must

also be recognized as an expense at NTCP 1.30 at the time of payment. There is therefore no accrual and deferral.

No. 31 requires, in addition to the evaluations known from IAS 1, an operating statement in which at least the following operating costs must be analyzed:

a) Raw materials

b) fuel

c) Electrical energy

d) Remuneration of the contract staff

e) depreciation of property, plant and equipment

f) Other monetary and financial expenses

It is not specified whether the consumption must be assigned to cost centers, cost objects, or a combination of both. It can then be assumed that this is left to the small business owner.

In addition to these comprehensive evaluations, the tax returns for the four types of tax mentioned in the income statement must also be prepared.

The bureaucratic requirements go far beyond what is required of small businesses in industrialized countries. It is understandable that most small business owners cannot do this. Without massive

technical and organizational support, the practical implementation of Articles 58 and 59 of the Taxes Act will not be possible.

3.3. Added value

In contrast to Germany, a Cost Accounting is also mandatory, unless simplified accounting (for cafes, restaurants, grocery, shoemaker) is permitted. However, it is also in the companies' own

interests to make their value creation process from investment, procurement, production and sales transparent. Bureaucratic regulations are rather a hindrance, because despite the similarities,

there are also special features for the individual industries. There is also a negative attitude towards a bureaucratic requirement which, in the opinion of small business owners, is in the

government's interest and cannot then be in their own interests. This prejudice can only be countered if, according to the Management Approach, the accounting information serves the management

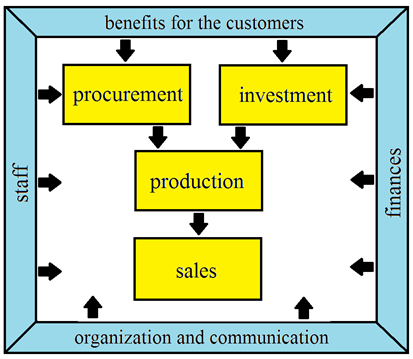

and this perspective of the management can also be seen in the external evaluations, e.g. in IFRS 8. The idea from Fig. 1 now continues.

Fig. 4: Value creation process

(Source: https://mueller-consulting.jimdofree.com/research/idea/background/)

Because of the legal requirement to analyze the operating expenses, it can also be expanded to an automated analysis of the value creation processes. The requirements of the Cuban NTCP 1.31 can

be easily reconciled with the German Operating Accounts Sheet (OAS) I and II. Based on concepts from the 1920s, they were created in the German decree on general principles of cost accounting

dated January 16, 1939. This is more about creating cost transparency and long-term planning than a basis for short-term decisions. The state regulation of cost accounting was one of the

preparations of fascist Germany for a state-controlled war economy. It was maintained by the occupying powers in the post-war period and was only lifted again in 1953. However, many companies

later retained the tools that were used for 14 years. It is understandable that a socialist state that permits private companies wants to keep control over the private sector of the economy and

then also uses tools that were developed for the same purpose in a fascist state.

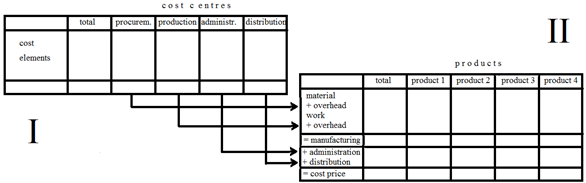

The OASs have the task of analyzing the input => production => output value chain. OAS I shows how the cost types (purchased goods) are distributed among the cost centers (organizational

units in which the added value takes place). Here, a distinction is made between direct costs that can be directly attributed to the products (cost objects) and the overhead costs, where this is

not possible. In contrast, OAS II deals with the contributions of the cost centers for the cost objects. Its procedure can be illustrated as follows:

Fig. 5: Operating accounting

(Source: own illustration)

A sample file with the name "hdg.ods" was offered for downloading for the project on the website https://www.oteninflation.de/cuba. The necessary formulas were stored in it and only the overhead

costs for the various cost centers have to be entered and the number of products produced and sold are recorded.

In the Open ERP concept, the analysis of operational costs stipulated in NTCP 1.31 can be carried out by specifying a purpose in addition to the cost type. The indication of the type of cost by

the small business owner does not have to correspond to the National Chart of Accounts from Annex 2 of Regulation No. 386-2010 of 30.12.2010. He can also provide his data with his own and simpler

number or letter code, which is automatically replaced by the number of the National Chart of Accounts after the upload. No binding cost center plan is provided for the analysis of operational

costs. This would not make sense because of the differences in the individual industries. However, the operator of an Open ERP system could work out proposals for various industries, which the

individual small business owner can then adapt to his needs.

The data collected by the small business owner can be copied into the "hdg.ods" data after uploading and processing in accounting. This would then result in an automated analysis of operational

costs in a quality that far exceeds the requirements of NTCP 1.31. Their goal is not only to meet bureaucratic requirements, but also to provide small business owners with information that

enables them to plan their activities effectively and improve profitability.

The procedure of the operational accounting sheet implements the system of total cost accounting. It is often criticized for not answering important questions such as the possibility of discounts

on large orders. However, small business owners rarely have the capacity to fulfill large orders. The questions that the system cannot answer in the critics' opinion therefore do not arise in

reality. In addition, the prices of small businesses are controlled by the provincial administrative councils. So their options are limited.

Although the analysis of operating costs is required by the state, the statements made in this analysis are geared internally. The entrepreneur wants to see which costs arise for which products

and product groups. The first question to be answered is whether he can cover his costs in the long term from the sales prices or whether he should not end this activity better. Conversely, he

also recognizes the products for which his costs are significantly lower than sales and on which he should therefore concentrate first. So first of all it is about the strategic direction of the

company. The activities with which the company can be successful in the long term must be identified.

In addition, there is the operational orientation to identify potential for cost reductions. The assignment of cost types to cost centers allows the question of whether this effort was really

necessary or whether the same service could not be organized with less effort. It is sufficient if only a few starting points for rationalization are identified. If opportunities for improvement

are continuously identified, this also increases the long-term success of a small company.

Finally, the analysis of operational costs also functions as an early warning system, which, however, requires the processed information to be processed quickly. Tendencies can be identified at

an early stage by comparing them with plans or at least evaluating previous periods. So one can analyze the causes at an early stage, reinforce positive tendencies and at least try to counter

negative tendencies. OAS II also takes sales into consideration. This enables opportunities to be better used and risks to be avoided better.

State regulation in this area is not helpful because of the importance of monitoring value creation processes by corporate management. It leads to the misconception that this observation is in

the interest of the government and not in its own interest. On the other hand, it is positive that no concrete analysis of the operating expenses was prescribed, which gives the small

entrepreneurs the necessary freedom. Small businesses would be completely overwhelmed with an independent implementation. An open ERP system has to organize the technical implementation with high

quality. Then the small business owners would only have to learn to understand the information and draw the right conclusions from it. The state, which most small business owners see as

opponents, could not organize these learning processes. An independent association of entrepreneurs could create the necessary trust.

3.4. business operations

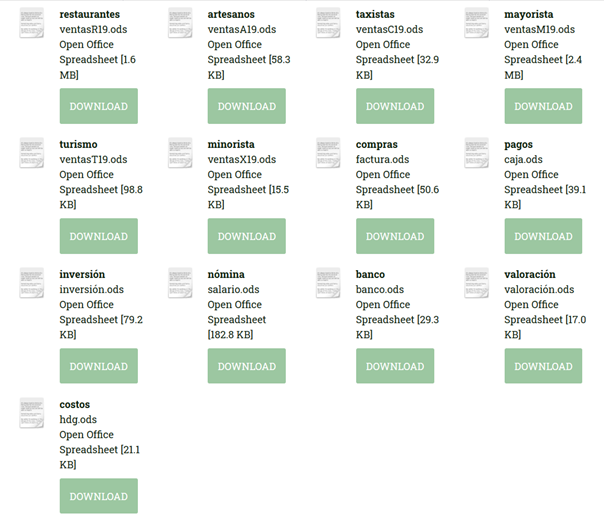

In the research project, the Open ERP concept was built up in modules in which the respective information was recorded with its own files. Of the 13 files that were created in the project and

offered for download on the Internet, 6 deal with the billing of orders from various industries. A small business owner only needs one of them. The remaining 7 files deal with issues that are

very similar in all companies.

Fig. 6: Download files from the project

(https://www.noteninflation.de/cuba)

The mass of data is generated in the companies in the operative business from purchasing and sales. An important question is the mandatory generation of receipts and invoices in some industries.

It would be an unnecessary duplication of work if the customer had to be immediately invoiced and the data from it was later manually transferred to the accounting department. However, there are

exceptions to this requirement.

When billing sales, the quantities sold are particularly important. The individual prices can be stored in the accounting file and then multiplied by the quantities sold. These sales can then be

recorded separately according to product groups.

There is a great need for many small business owners not to include all sales in official accounting. The tax deduction ban for expenses paid in cash should act like a cash payment ban for

companies. Because it is unavoidable in some industries to make purchases in cash, part of the cash sales are not officially billed to finance these cash purchases. In restaurants, it is

considered rude to take the waiter's invoice with you after payment. This gives the owners the opportunity to make the copy disappear again. Even very well attended restaurants, where guests have

to wait for a free table, are officially only half full. So much turnover is posted that the cashless purchases appear plausible. Records of other sales should be avoided. The criticism of the

party newspaper was therefore quite justified, but the shadow economy is also reinforced by the factual ban on cash payments. This dual approach also inhibits the use of modern accounting

systems.

In the "maestra" worksheet in the "factura.ods" file, 26 codes were initially stored with capital letters for processing purchases on account, which can be used to define common uses. Below that,

the account no. and account name and the bookings currently in this file are displayed. This code is entered in the worksheet "entrada", after which account no. and the account name behind it are

automatically displayed. You can also enter a two-digit cost center number and a three-digit cost object number that changes from the table in column N to a five-digit cost center number to be

merged into an accounting program for data transmission. Without data transmission, the data can also be sorted according to the entered codes. To do this, the data area should be copied to

another file. The own invoice number. will continue automatically. For this, the last invoice number from the previous file has to be entered.

Entering the purchase per invoice, payment must already be considered. In anticipation of electronic banking, which was introduced in December 2017 (https://cubaheute.de/tag/bpa/) but has not yet

been expanded across the board, the file has an application of the international bank account no. (IBAN) assumed. For this, the IBAN and the name of the vendor must be registered and it appears

when the vendor number will be entered. In addition, the invoice number used by the vendor is required for later payment. The name and IBAN are stored under this number in the maestra

worksheet.

In addition to the table of the recorded invoices, there is a table with the codes, account number and name as well as the bookings currently accumulated in this file. This part helps to enter

the correct letter as the code for the account number. To the right there is a table with the names of the creditors and the IBAN, which next to the invoice number of the vendor and the amount

needed for the payment.

For purchases that are paid for immediately, you can pay with cash, a bank card or a credit card. These three payment methods must be separated and the current cash balance or the remaining

credit card credit limit updated. Purchases paid for in cash are operationally initiated even without tax recognition. However, they are more likely to be paid from undeclared earnings and then

not booked. A separate table was developed for this.

The intended use can again be shortened to 26 letters. Because it is regularly a question of specific expenses that must be paid for immediately using cash or a card, the stored account numbers

can differ from the invoices. It therefore makes sense to place an explanation of the short codes next to the data entry. The definition as cash, bank or card payment is also made with a letter.

However, a number can also be used. Two further definitions are to be provided for the transfer of bank credit to the credit card and for cash withdrawals from the bank account. The document no.

will be continued automatically. It makes sense to keep a separate file for each month, whereby the period is integrated into the document number and can otherwise start again every month.

The small business owners first watch the cash flows. A table was therefore created with which an original cash flow statement can be produced from the bank accounts using the direct

method.

First, the amounts with the date of payment are transferred to a table in the "entrada" worksheet, with deposits and withdrawals being entered in two separate columns. This can also be done using

data import. The current account balance is calculated in the "Balance" column. As with incoming invoices, the payments are assigned to the various cash flows using a letter. A comment can also

be added. Most payments will be assigned to groups A (de clientes - from customers) and B (a proveedores - to suppliers). Group M can also be defined for investments. In column D, the invoice

number is detected. The assignment to the cash flows already results in a separation into incoming and outgoing invoices. The data in the cash flow statement in the worksheet "presentación" are

derived from the data in the bank accounts.

Multiple bank accounts can be processed. A table with the current sums of cash flows, which was arranged next to the data entry table, is controlled from the "maestra" worksheet. They are then

completed by the data of the cash registers, which can be completely assigned to groups A (income from a store cash register) and B (small cash expenses in a subsidiary cash register).

The original procedure has the advantage that an evaluation is possible very quickly without having to go through accounting. The data recorded here can rather be imported into the accounting

itself.

The companies in Guantánamo were not very informative when it came to personnel deployment. It can be assumed that part of the personnel costs are paid from undeclared earnings and that more

employees can be employed than were registered. The payments social security contributions for employees and personal income tax are covered by taxes for the company. A special problem in the

recording of personnel costs is therefore not seen.

The NTCP 1 does not provide a valuation that deviates from the payments. Small businesses see no practical application for the file valoración.ods, which can be used to record such deviations.

Cost accounting with the hdg.ods file has already been discussed in the previous section.

3.5. Data transfer

Data transfer to financial accounting software can be organized from the ods files by creating a table in a separate worksheet according to the software specifications, which can be saved as a

text file and then imported into the software. This can be organized by uploading via the Internet. The following booking records result from the ods files:

ventasR19.ods debit cash, credit sales

ventasX19.ods debit cash, credit sales

gross profit (=> debit expense, credit inventories)

purchase of goods (=> debit Inventories, credit cash / bank / [liabilities])

ventasA19.ods debit [receivables], credit revenues

ventasC19.ods debit cash, credit sales

debit fuel, credit cash

debit car costs, credit cash

debit private withdrawal, credit offsetted vehicle costs

tax, insurance, depreciation

ventasM19.ods debit [receivables], credit revenues

ventasT19.ods debit bank / cash register / credit card, credit sales

caja.ods debit [expenses or assets], credit cash / bank / Credit C.

factura.ods debit [expenses or assets], credit [liability]

salario.ods debit personnel expenses, credit liability

banco.ods debit bank, credit [receivables]

debit Bank, credit [Yield or Debt]

debit [Liabilities] , credit bank

debit [Expense or assets], credit bank

inversión.ods debit fixed assets, credit offset

debit depreciation, credit fixed assets

debit expenses from asset disposals, credit fixed assets

debit fixed assets, credit income from asset disposals

debit interest expense + loan, credit bank

debit offsetting, credit loans

debit

imputed depreciation, credit calculated imputed costs

debit

imputed interest, credit calculated imputed costs

valoración.ods debit cost of materials, credit inventories (old)

debit Inventories, credit cost of materials (new)

debit

Inventory changes, credit inventories (old)

debit

Inventory, credit Inventories (New)

debit

Expenses, credit value adjustment

debit Value

adjustment, credit [claim]

debit Value

adjustment, credit other operating income

debit other

claim, credit [yield]

debit

Prepaid expenses, credit [expense]

debit

[Expense], credit other liability

debit

[Income], credit deferred income

debit Tax

expense, credit tax provision

debit other

receivable, credit tax

debit

[Expense], credit provision

debit

Provision, credit [expense] or bank / cash

debit

Provision, credit other operating income

debit imp.

entrepreneurial wage, cred. offseted imp. costs

debit

imputed rent, credit offseted imputed costs

debit

imputed risks, credit offseted imputed costs

hdg.ods no accounting

The information in square brackets is specified in the ods file.

The intended evaluations, automatically booked accounts and automatically generated evaluations, in particular the balance sheet, the profit and loss account and the cash flow statement, can be

created from uploaded files. For internal accounting, the OAS I and II has already been presented in the hdg.ods file. An evaluation created from the accounting software would no longer be

absolutely necessary for this.

Alternatively, the files ventas?19.ods, caja.ods, factura.ods, salario.ods, banco.ods, inversión.ods and valoración.ods could also be copied into a common file and then another worksheet for

balance sheet, profit and Income statement and cash flow statement can be added. File references can also be set. This would have to be designed individually for the respective company.

3.6. Future data

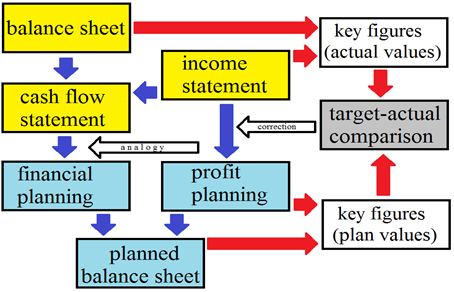

The accounting standards can only regulate the presentation of the past. However, companies are led into the future, and entrepreneurs should be interested in comparing past data in the same

format with expectations and plans for the future. With the application of key figures, the current economic situation is also compared with the past and the amounts resulting from the corporate

planning can be evaluated according to the same logic. If the key figures resulting from the planning are not satisfactory, you can respond by changing the planning. This results in the following

control loop:

Fig. 7: Interaction between actual and planned values

(Source: own illustration)

In the materials for a digital course, the author presented an example in German in the file Fallstudie.pdf on the website https://www.prof-mueller.net/lehrveranstaltungen/grundzüge/.

For the past, the quantities produced, sold or consumed and the amounts from sales and expenses are required as a planning basis. The division of the amount by the quantity results in a price or

a unit cost rate. In the case of very heterogeneous expense items, an artificial unit of measure can be created by dividing the amount by a price index.

Fig. 8: Past and future

|

|

monetary units |

price |

quantity units |

|

Past |

|

|

|

|

direct |

amount accord. to accounting |

amount : quantity |

statistics |

|

Or |

|

|

|

|

derived |

amount accord. to accounting |

index value |

amount : price |

|

future |

quantity × price |

past × index |

past × expectation |

italics = data required

(Source: own illustration)

These figures can be updated in the future with your own expectations with regard to volume development and price development. This is done in stages according to the following planning

scheme:

quantity price

amount

actual actual quantity actual price

actual cost

- not applicable - actual quantity actual price - actual costs

= remaining = remaining quantity actual price = remaining actual costs

+ additional + partial plan quant. actual price

= basis planned quantity actual price

+ change of prices plan quantity price diference

= plan plan quantity plan

price plan costs

Small business owners cannot organize business planning without expert advice, not even with planning software. The management consultants who offer such support treat their formula collections

as a trade secret. A business association that would implement the Open ERP concept presented in this article would be able to exchange its knowledge nationwide and thus ensure that, as a result,

every small business owner can learn from everyone's experience.

4. Outlook

The political conditions have significantly limited the scope of the findings from the research project from the summer semester 2019. Nevertheless, insights have been gained that may be used to

strengthen small business owners in other Latin American countries. With the approval of an independent association of small business owners, socialist Cuba would have the potential to organize

this segment of its economy efficiently and to use the Open ERP concept to develop and use a technology that it could then export to other countries. In non-socialist countries, this concept

would first have to be organized and financed by the private sector.

But it is also not impossible that governmental economic policy wants to promote small entrepreneurs and that the organization could take over. This essay could help to spread such a

proposal.

Sources:

COMMISSION OF THE EUROPEAN COMMUNITIES, COMMISSION REGULATION (EC) No 1126/2008 of 3 November 2008 adopting certain international accounting standards in accordance with Regulation (EC) No

1606/2002 of the European Parliament and of the Council, Official Journal of the European Union as of Nov. 29, 2008

CUBAHORA. Primera revista digital de Cuba, Centro de Información para la Prensa:

https://www.cubahora.cu/economia/trabajo-por-cuenta-propia-una-cronologia-de-preguntas-y-respuestas

Dirk Jödicke, Düsseldorf, http://eu-ifrs.de/wp-content/uploads/EU-IFRS_2020.pdf

Marcel Kunzmann, Berlin, Einkaufen auf Kuba wird billiger – mit Kartenzahlungen, https://cubaheute.de/tag/bpa/, 03.05.2018

MINISTERIO DE JUSTICIA DE LA REPUBLICA DE CUBA:

LEY No. 113 del Sistema Tributario, Gaceta Oficial No. 053 Ordinaria de 21 de noviembre de 2012

Resolución No. 904/2018 del Ministerio de Finanzas y Precios, Gaceta Oficial No. 77 Extraordinaria de 5 de diciembre de 2018

Resolución No. 386/10 del Ministerio de Finanzas y Precios, Gaceta Oficial No. 038 Extraordinaria de 30 de diciembre de 2010

Mondial21 e. V., Berlin: https://Amerika21.de/2019/12/235503/mobiles-netz-kuba-touristen; 17 de diciembre de 2019

Werner Müller, Mainz:

https://mueller-consulting.jimdofree.com/research/history/

https://mueller-consulting.jimdofree.com/research/accounting-3-0/

https://mueller-consulting.jimdofree.com/research/idea/background/

https://www.prof-mueller.net/lehrveranstaltungen/grundzüge/

https://www.noteninflation.de/cuba

Progreso Weekly Inc., https://progresosemanal.us/20180227/activan-contabilidad-simplificada-actividades-privadas/, 16.05.2018