deutsche Fassung

Version en español

Русская версия

Version française

5.2. evaluations

It has already been formulated as the goal that monthly data of a balance sheet, income statement and cash flow statement, as well as a simple cost and activity accounting with cost type

accounting (especially with the entry of imputed costs), cost center accounting (for cost control) and cost unit accounting (for the Price and product policy) should be generated. It must first

be checked which contents are specifically required for this.

5.2.1. balance sheet

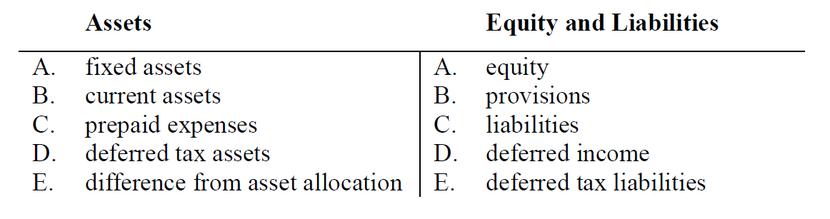

In Section 266 of the German Commercial Code (HGB), the content of the balance sheet for Germany is defined as a sample structure for large corporations. For medium and small corporations a

reduced scope applies. For private companies there is no legally prescribed structure. Nevertheless, they are expected to be able to answer questions about content from the Deep Subdivision.

Under the system of 1494 a distinction is made between the asset side with the representation of the assets and the liability side with the representation of the capital. The rough classification

for small chapter companies has the following scope:

Fig. 32: Balance sheet according to § 266 HGB

(Source: own illustration)

The positions C to E of the asset side and D and E of the liability side are not further broken down; only one of the deferred items is required (including discount according to § 250 (3) HGB).

These positions do not arise from the current business activity but from valuations during the financial statement. Deferred items can also be updated during the course of the year. For example,

for the preparation of monthly and quarterly financial statements. Provided that the relevant facts are identified, an automatic booking is also possible. On the other hand, taking account of

deferred taxes during the year makes little sense, because the taxes are annual amounts. One would fictitiously assume a monthly tax assessment.

The complete version of the fixed assets has the following scope:

Fig. 33: Fixed assets in accordance with § 266 (2) HGB

|

A. |

fixed assets |

|

I. |

intangible assets |

|

1. |

self-created industrial property rights and similar rights and values |

|

2. |

licenses acquired for a consideration, industrial property rights and |

|

|

similar rights and assets as well as licenses to such rights; and values |

|

3. |

goodwill |

|

4. |

advance payments |

|

II. |

property, plant and equipment |

|

1. |

land, land rights and buildings including buildings on strange land |

|

2. |

technical equipment and machinery |

|

3. |

other equipment, fixtures and fittings |

|

4. |

advance payments and assets under construction |

|

III. |

Investments |

|

1. |

shares in affiliated companies |

|

2. |

loans to affiliated companies |

|

3. |

shares in other companies |

|

4. |

loans to companies with which shares are held |

|

5. |

securities of fixed assets |

|

6. |

other loans |

(Source: own illustration)

The complete version of the current assets has the following scope:

Fig. 34: Current assets pursuant to § 266 (2) HGB

|

B. |

current assets |

|

I. |

supplies |

|

1. |

Raw materials and supplies |

|

2. |

work in progress |

|

3. |

finished products and goods |

|

4. |

advance payments |

|

II. |

Receivables and other assets |

|

1. |

Trade receivables |

|

2. |

receivables against affiliated companies |

|

3. |

receivables against companies with participating interest |

|

4. |

other assets |

|

III. |

Securities |

|

1. |

shares in affiliated companies |

|

2. |

other securities |

|

IV. |

Cash on hand, Central Bank balances, credit balances with |

|

|

banks and checks |

In the case of receivables (II), the note "thereof with a remaining term of more than one year" must be made.

(Source: own illustration)

The complete version of the debt capital has the following scope:

Fig. 35: Liabilities according to § 266 (3) HGB

|

B. |

Provisions |

|

1. |

Provisions for pensions and similar liabilities |

|

2. |

Tax provisions |

|

3. |

other provisions |

|

|

|

|

C. |

Liabilities |

|

1. |

bonds |

|

|

of which convertible |

|

2. |

liabilities to banks |

|

3. |

advance payments received on orders |

|

4. |

trade payables |

|

5. |

liabilities arising from the acceptance of commercial |

|

|

bills and the issuance of own bills |

|

6. |

liabilities to affiliated companies |

|

7. |

liabilities to companies with participating interest |

|

8. |

other liabilities |

|

|

thereof taxes |

|

|

thereof in the context of social security |

For all liabilities (C) are in addition the notes

- of which with a residual maturity of up to one year

- thereof with a remaining term of more than one year

under the position.

(Source: own illustration)

Provisions are insecure liabilities that have been calculated by themselves.

The small businesses must align their data collection to the extent relevant to them. Irrelevant positions can be omitted. Bonds can not exist in small businesses. Affiliated companies and

participations exist only if the operational functions were split over several companies. Commercial are only common in international trade.

The full version of the equity capital has the following scope:

Fig. 36: Equity pursuant to § 266 (3) HGB

|

A. |

Equity |

|

I. |

drawn capital |

|

|

less pending deposits |

|

|

less own shares |

|

II. |

capital reserve |

|

III. |

retained earnings |

|

1. |

legal reserve |

|

2. |

reserve for shares in a ruling company involved |

|

3. |

statutory reserves |

|

4. |

other reserves |

|

IV. |

profit carried forward / loss carried forward |

|

V. |

net profit or loss |

(Source: own illustration)

It should be clearly separated between deposits and retained profits. In the case of private companies, the equity is allocated to the persons. Again, there is the separation between deposit and

retained profits.

5.2.2. Income statement

The full version of the profit and loss account according to the total cost method has the following scope:

Fig. 37: Profit and loss account according to § 275 Abs. 2 HGB

|

1. |

Sales |

|

2. |

increase or decrease of stock of finished and unfinished products |

|

3. |

other own work capitalized |

|

4. |

other operating income |

|

5. |

material expenditure |

|

a) |

expenses for raw materials and supplies and for related goods |

|

b) |

expenses for purchased services |

|

6. |

personnel expenses |

|

a) |

wages and salaries |

|

b) |

social charges and expenses for pensions and for assistance |

|

|

of that for pensions |

|

7. |

Depreciation |

|

a) |

on intangible assets and property, plant and equipment |

|

b) |

on assets held as current assets; as far as these exceed the |

|

|

customary depreciation in the capital company |

|

8. |

other operating expense |

|

9. |

income from investments |

|

|

thereof from affiliated companies |

|

10. |

income from other securities and loans of financial assets |

|

|

thereof from affiliated companies |

|

11. |

other interest and similar income |

|

|

thereof from affiliated companies |

|

12. |

depreciation on financial assets and on securities |

|

|

held as current assets |

|

13. |

Interest and similar expense |

|

|

thereof from affiliated companies |

|

14. |

Taxes on income |

|

15. |

Earnings after taxes |

|

16. |

other taxes |

|

17. |

net profit or loss |

(Source: own illustration)

Again, there will be some irrelevant positions.

Position 8 also includes overheads. They can be very different. The company is likely to be interested in a breakdown. The specific positions are also dependent on the industry.

5.2.3. Cash Flow Statement

For many small businesses, cash flows are closer and easier to understand than the income statement or balance sheet items. The direct method, which is also recommended by IAS 7.19, meets this

need. Reference is made to the comments in section 3.6.

IAS 7 does not contain a sample structure. According to German Accounting Standard No. 21 (DRS 21), however, the following structure may be proposed, which may also contain irrelevant items:

Fig. 38: Cash flow statement according to DRS 21.39, 46, 50

| Cash flow from operating activities |

|

1. |

Received payments from customers for the sale of products, |

|

|

goods and services |

|

2. |

– payments to suppliers |

|

3. |

– payments for employees |

|

4. |

– Payments for VAT and other taxes |

|

5. |

+ Other deposits, other than investment or financing activities |

|

6. |

– Other payments, other than investment or financing activities |

|

7. |

–/+ income tax payments |

|

8. |

= cash flow from operating activities |

Cash flow from investing activities

|

1. |

deposits from the disposal of objects of the intangible assets |

|

2. |

– payments for investments in the intangible fixed assets |

|

3. |

+ deposits from disposals of objects of the rixed assets |

|

4. |

– payments for investments in property, plant and equipment |

|

5. |

+ Deposits from the disposal of objects of the financial assets |

|

6. |

– payments from the repayment of bonds and (Financial) loans |

|

7. |

+ deposits due to financial assets as short-term fin. management |

|

8. |

– payments due to financial investments as short-term |

|

|

financial management |

|

9. |

+ interest received |

|

10. |

+ dividends received |

|

11. |

= cash flow from investing activities |

Cash flow from financing activities

|

1. |

deposits from equity contributions |

||

|

2. |

+ deposits from the issue of bonds and bonds the admission |

||

|

|

of (financial) credits |

||

|

3. |

– payments from the repayment of bonds and (Financial) loans |

||

|

4. |

+ deposits from grants / grants received |

||

|

5. |

– paid interest |

||

|

6. |

– paid dividends |

||

|

7. |

= cash flow from financing activities |

||

|

|

total cash flow |

|

|

|

|

+ opening balance of cash and cash equivalents |

|

|

|

|

= ending balance of cash and cash equivalents |

|

|

(Source: own illustration)