deutsche Fassung

Version en español

Русская версия

Version française

5.2. evaluations

It has already been formulated as the goal that monthly data of a balance sheet, income statement and cash flow statement, as well as a simple cost and activity accounting with cost type

accounting (especially with the entry of imputed costs), cost center accounting (for cost control) and cost unit accounting (for the Price and product policy) should be generated. It must first

be checked which contents are specifically required for this.

5.2.4. Cost element calculation with imputed costs

The cost element number transfers the accounting data to the cost accounting module, whereby several G / L accounts are added up under this number. Thus, a completely independent structure can be

created. To avoid processing errors, all G / L accounts should be assigned cost types. This also includes cost types for neutral expenditure, assets and capital.

In a research project in the winter semester 2014/15, the author has developed and proposed the following cost plan:

Fig. 39: Cost element plan from research project

|

1st digit |

|

2nd digit |

at 4-8 |

|

1 |

assets |

0 |

material costs + subcontractors |

|

2 |

capital |

1 |

bought goods + services |

|

3 |

income |

2 |

personnel costs |

|

4 |

proportional |

3 |

personnel-related costs |

|

5 |

variable |

4 |

operating costs |

|

6 |

partially fixed costs |

5 |

room costs |

|

7 |

interval fixed costs |

6 |

vehicle- / travel costs |

|

8 |

fixed cost |

7 |

administrative costs |

|

9 |

neutral costs |

8 |

typical cost of sales |

|

|

1? Assets |

|

2? capital |

|

10 |

intangible assets |

20 |

Equity |

|

11 |

real estate + ass. under construction |

21 |

Provisions |

|

12 |

technical equipment + machines |

22 |

Bonds |

|

13 |

other plants, operational equipment |

23 |

bank liabilities |

|

14 |

vehicles + office equipment |

|

|

|

15 |

financial assets + neutral assets |

25 |

trade payables |

|

16 |

Inventories |

26 |

group liabilities |

|

17 |

Receivables |

27 |

other liabilities |

|

18 |

securities + liquidity |

28 |

liabilities from tax and levies |

|

19 |

delimitation |

29 |

delimitation |

|

3rd digit |

at 4-8 |

4th digit |

at 4-8 |

|

0 |

direct costs |

0 – 6 |

expenses equal |

|

1 |

special direct costs |

7 |

normalized |

|

2 - 9 |

Overheads |

8 |

imputed |

|

|

|

9 |

secondary |

2.+3. digit at class 4-8

|

No. |

designation |

No. |

Designation |

|

0 |

production materials |

52 |

rent + utilities |

|

1 |

subcontractors use |

53 |

occupancy costs |

|

2 |

indirect material |

54 |

cosmetic repairs |

|

3 |

consumption auxiliaries |

55 |

repairs |

|

4 |

consumption of consumables |

58 |

property taxes |

|

5 |

machine power |

59 |

depreciation on buildings |

|

10 |

expenses for purchased goods |

61 |

travel costs settled with customers |

|

11 |

spec. direct costs in production |

62 |

variable vehicle costs |

|

13 |

disposal costs |

63 |

fixed vehicle costs |

|

17 |

hall energy |

65 |

mileage allowance employees |

|

20 |

direct costs wages |

66 |

train + plane tickets |

|

21 |

salesmen commissions |

67 |

lumpsum travel expense |

|

22 |

overheads wages |

72 |

legal and consulting fees |

|

23 |

wages |

73 |

office expenses |

|

24 |

pensions |

74 |

postage, telephone |

|

25 |

legal social expenditure |

75 |

IT costs |

|

26 |

voluntary social effort |

76 |

leasing business equipment |

|

32 |

workwear |

76 |

fees |

|

39 |

various staff costs |

78 |

membership in organisations |

|

40 |

effort for waste products |

79 |

deprec. on prop, plant and equipment |

|

41 |

special tools |

81 |

special expenses of distribution |

|

42 |

small tools |

82 |

packing material |

|

44 |

repairs |

83 |

write-downs on claims |

|

45 |

wear parts |

85 |

catering + Representation |

|

46 |

maintenance |

86 |

Giveaways |

|

47 |

machine leasing |

87 |

Advertising |

|

48 |

various commercial costs |

88 |

Gifts |

|

49 |

deprec. o. prop., plant + equipm. |

89 |

other typical distribution costs |

93 risks 95 interest

97 taxes 99 offsetting

(Source: own illustration)

Imputed costs must also be recorded in the accounting department. Here, a separate account group is maintained, in which bookings and offsetting postings cancel each other out. In cost

accounting, the clearing accounts for the offsetting postings are assigned to a neutral cost element. For other costs, which are to be supplemented by imputed cost types, the effort can be

treated as a neutral expense and the cost element can be calculated independently.

5.2.5. cost center accounting for cost control purpose

For cost centers as part of internal accounting, there are no requirements and only a few generally applicable recommendations, such as the Federal Association of German Industry. In Fig. 15 on

page 74, a system for cost center numbers has already been discussed. The BDI proposal would look like this according to this system:

Fig. 40: BDI proposal for cost center plan

0. non-operating activities

01 Rental

03 utilization of rights

05 Securities Trading

1. Material cost centers

10 Material Management in general

11 ordering

quotation processing, ordering, scheduling, material

groups,

13 Goods acceptance and inspection

receiving, incoming goods inspection, warehouse overhaul,

permanent inventory

15 Material Management

Stock accounting, material planning

17 Material storage and issue

Raw material storage, parts storage, tool storage, tool dispensing,

external store, scrapyard

19 transport

lorries, electric carts, railway tracks, petrol

stations

2. Research and Development / indirect manufacturing Cost Centers

20 technique, general

22 Research and Development

Research, development, process experiments

23 construction

Standardization, subscription registration

24 trials, testing

Testing laboratories, test fields, material testing

25 prototype construction and testing

functional patterns, exhibition patterns

27 production preparation

production and equipment planning, work and time studies,

quality control

28 production control

production technology, company office, equipment manufacturing,

interim storage, tool storage

3 to 6. main production cost centers

30 prefabrication

40 main manufacturing

50 installation

60 Special Production

7. Distribution Cost Centers

70 Sales in general

71 sales preparation

Market research, product information, sales planning,

advertising

72 acquisition / sale

field service, branches

73 order processing

Order processing, invoicing

74 finished goods warehouse, packaging and

shipping

Packing, shipping

75 Customer Service

8. General and Administrative Costs

80 General Administration

81 Management

management, press office

82 personnel administration

payroll, suggestion system, Training, social affairs

83 Finance and Accounting

General Ledger, Current Account, Finance, asset accounting,

cost accounting, costing, evaluation and controlling

84 special administrative services

law, taxes, organization, audit, corporate planning, EDP,

patents

85 General Administration

telephone switchboard, in-house mail, registry, translation agency,

office supplies, duplication

86 General factory service

plant protection, fire department

87 social services (company

doctor, sports facilities, library,

canteen, Recreation Center, workers council)

9. Auxiliary cost centers of the general items

91 land and buildings

land, factory buildings, commercial buildings, warehouse buildings,

residential buildings, barracks

92 power supply (water supply, steam supply,

heating

system, power station, gas supply)

93 maintenance

maintenance machinery and tools, building maintenance,

maintenance electrical systems

(Source: own illustration)

This plan can be adapted to the individual conditions. Thus, as an alternative to the BDI proposal, human resources management (82) could be run as an auxiliary cost center (for example 94), the

costs of which would be distributed among the employed workers. Accordingly, the data processing could be charged according to the devices used.

Small businesses will reduce the scope.

Following the suggestion from Fig. 15 on page 74, the cost centers between 10 and 79 in the last 3 digits of the five-digit cost center no. awarded with a cost object identifier. The cost center

numbers beginning with 0, 8 and 9 can be assigned with 5 digits.

Fig. 41: Account number

(Source: own illustration)

An exception to the limitation to 2 digits are the cost places, which should have a 9 in the 3rd position. The cost center no. 22903 would be in the research for the machine (= cost place) 3

(question where? - cost center). On the other hand, No. 22803 would be a research project for product 3 of product group 8 (question for what? - cost object).

The projects and work orders are treated as payers. Would e.g. Defining a party for a company anniversary as a project, one wants to determine the costs of this celebration. However, they are not

paid by the visitors but are overhead costs through the cost center of the company management.

5.2.6. Cost unit accounting for the price and product policy

The cost center numbers can only cover individual costs of the different products. If individual items can also be assigned to cost objects that would otherwise be allocated to overhead costs,

these amounts would be special costs.

The website https://mueller-consulting.jimdo.com/finances/costs/ branches to the download file BAB-Muster.ods from the website https://www.noteninflation.de/downloads, where with the allocation

of costs Types of Cost Center Groups (Columns in a BAB - Operating Statement Sheet), the relationships between overhead costs and direct costs are calculated.

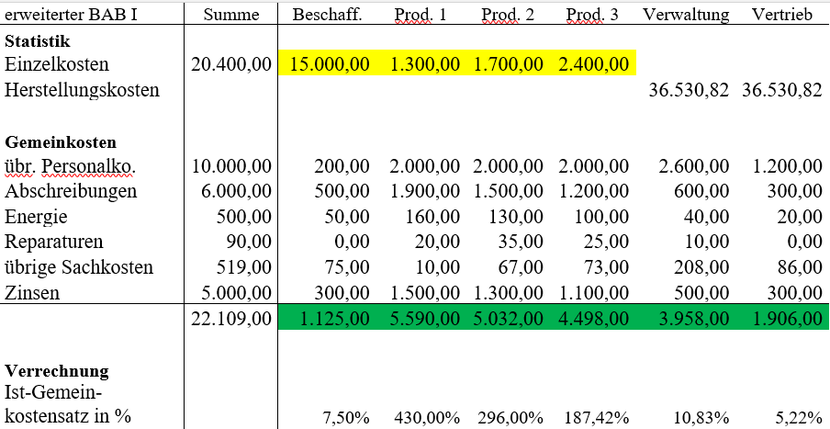

Fig. 42: Operating statement sheet I

(Source: Download file BAB-Muster.ods - There is only a German version.)

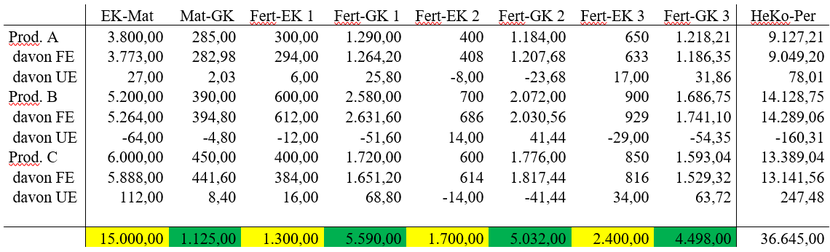

With the direct costs per product and the actual overhead rates, the production costs of the period, broken down into finished goods and work in progress, are calculated in an Operating Statement

Sheet II.

Fig. 43: Operating statement sheet II

(Source: Download file BAB-Muster.ods - There is only a German version.)

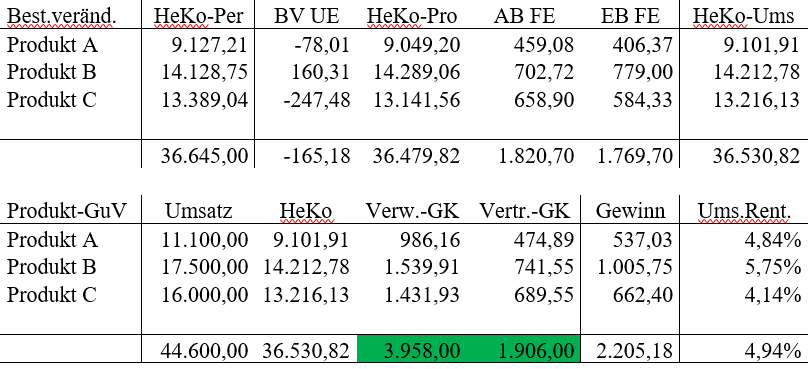

Subsequently, the production costs of production are determined, taking into account the changes in inventories of work in progress, and the manufacturing costs of sales are taken into account

after taking into account changes in inventories of finished goods. In a product profit and loss account according to the cost of sales method, the profit after deducting the production costs,

administrative and selling overhead costs is then calculated.

Fig. 44: Changes in inventories and product income statement

(Source: Download file BAB-Muster.ods - There is only a German version.)

With a determination of the profit up to the level of the individual products the central question for the success of an enterprise is answered. The company management wants to concentrate on the

profitable products, which must be identified first.